Someone is arguing on Reddit about two Vanguard funds that are almost the same.

That’s the part nobody tells you at the start of this debate. VTSAX and VOO are buy-and-hold investments, and it’s best not to think about them. Both are from Vanguard, which is essentially the creator of boring and inexpensive investing. So, when you take a look under the hood, approximately 87% of what you have in VTSAX is the same as what you’d have in VOO. Same companies. Same weightings, roughly. The same low-cost approach of the same Vanguard.

If you’re wondering, that’s why it creates thousands of comment threads where people insist that their favorite choice is the smarter one.

The other 13%, plus some subtle differences in taxes, structure, and fees, and many of the things people discuss about them online are either outdated or simply incorrect. This article is going to sort out what’s real. At the end, you will know the difference between VTSAX vs VOO: It’s not what most people believe it to be!

Quick answer

In terms of the short story, the returns of VOO have been slightly higher in the past 5 and 10 years, but VTSAX has managed to outperform in the past 12 months. Both funds are “right”! VOO provides you with the 500 largest U.S. companies. VTSAX offers you the same companies with a portion of smaller companies thrown in. The real decision isn’t performance; it’s whether you want that extra slice.

| Metric | VTSAX | VOO |

| Structure | Mutual fund (Admiral shares) | ETF (exchange-traded fund) |

| Tracks | CRSP US Total Market Index | S&P 500 |

| Expense ratio | 0.04% | 0.03% |

| Minimum investment | $3,000 | 1 share (~$687) or $1 fractional |

| Holdings | 3,484 companies | 505 companies |

| 10-year return (as of 6/30/2026) | 15.03%/yr | 15.47%/yr |

| 1-year return (as of 6/30/2026) | 23.15% | 22.28% |

| 30-day SEC yield | 1.01% | 1.03% |

| Capital gains distributions | None since 2000 | None (ETF structure) |

| ETF / mutual fund twin | VTI | VFIAX |

Data: Vanguard, as of 6/30/2026 (returns) and 5/31/2026 (portfolio characteristics).

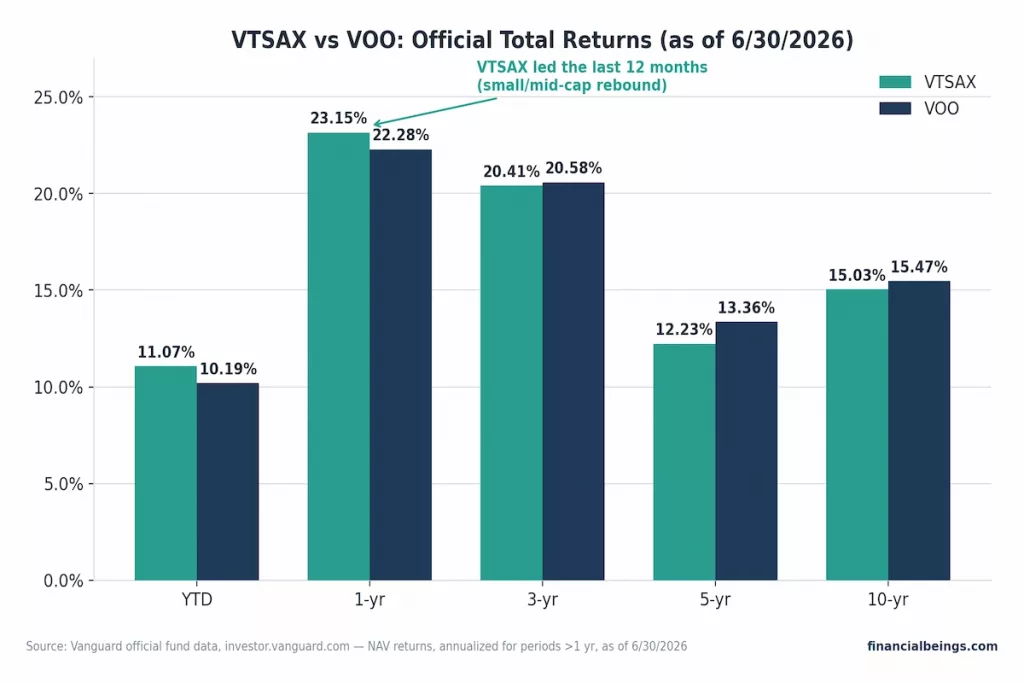

Performance: The 10-Year Data (and the Last 12 Months)

| Period | VTSAX | VOO |

| YTD | 11.07% | 10.19% |

| 1-yr | 23.15% | 22.28% |

| 3-yr | 20.41% | 20.58% |

| 5-yr | 12.23% | 13.36% |

| 10-yr | 15.03% | 15.47% |

Let’s get acquainted with our example. Suppose that there is a person named Marcus. He’s 34 years old, has $10,000 in a brokerage account, and is considering where to invest that money. He has heard that VOO is safer and proven. He has heard about the ‘more complete’ option being VTSAX. He wants stats; he doesn’t care about the hype.

Here are the facts based on the numbers as of June 30, 2026. VOO has averaged 15.47% a year for the past 10 years. Over the past 10 years, VTSAX has seen a return of 15.03%. Over 5 years, the gap is similar: VOO at 13.36%, VTSAX at 12.23%.

Over 3 years, they’re nearly tied: 20.58% versus 20.41%. But, over the past year, something out of the ordinary occurred: the VTSAX fund beat VOO, 23.15% vs 22.28%. Year-to-date, VTSAX is ahead too, 11.07% to 10.19%.

That flip is a story worth paying attention to. For most of the last decade, big companies, the kind that dominate the S&P 500, outran everyone else. Investors desired safety, scale, and the behemoth tech companies that are packed into VOO.

Those smaller/mid-size companies began to close the gap over the past year, and some investors are referring to it as “rotation”. If you’re curious how a momentum-based approach stacks up against this same S&P 500 benchmark, our SPMO vs VOO comparison breaks that down. If that occurs, companies that don’t have many of VOO’s holdings, as thousands of smaller companies do in a fund such as VTSAX, benefit, but VOO does not.

Who knows what will happen with that rotation next quarter or if it will continue. That’s pretty honest, and anyone promising you otherwise is up to something.

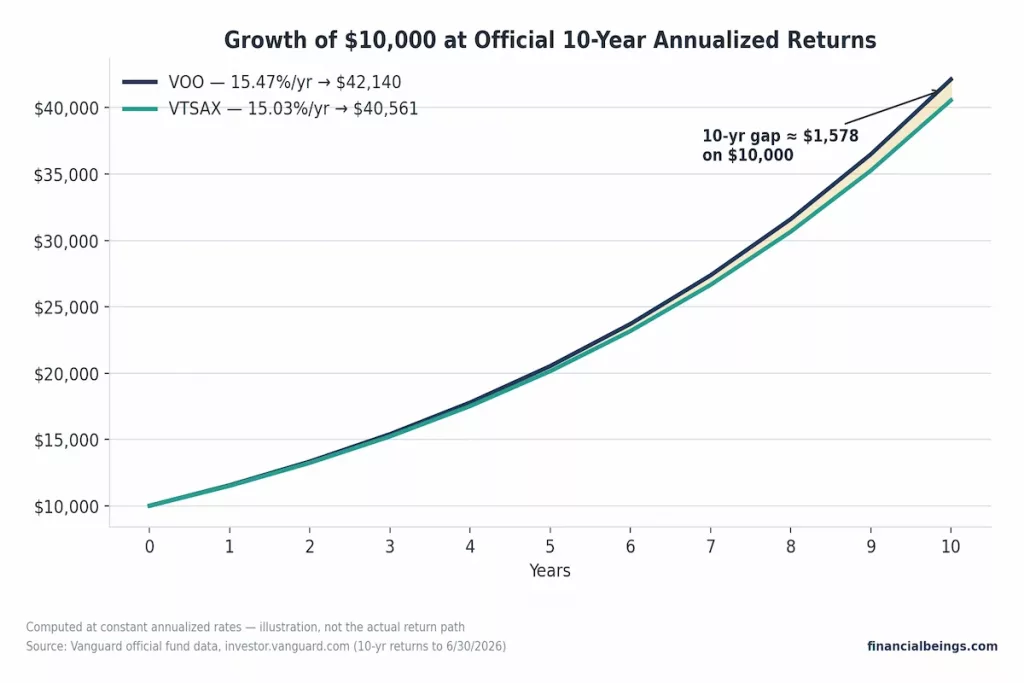

Now, let’s put this in dollars, because percentages are slippery and dollars are not. If Marcus invested $10,000 in both funds and compounded the earnings at the annual rate of each fund, over 10 years, the value of VOO would have been $42,140. The value of VTSAX would have risen to $40,561. This is about $1,578 for a 10-year timeframe from a starting point of $10,000.

It’s not a matter of ‘things that aren’t real money’, so much as it is a matter of ‘things that aren’t the difference between a comfortable retirement and no retirement at all’. Now it’s important to state up front that the dollar number is a projection, not the actualroute the two funds took to reach that number. The real markets don’t go in a straight line.

What You Actually Own: Quality vs. Price

Most comparison articles don’t get into this; here’s one way to think of the funds: each is one company in which you are purchasing a stake; ask yourself what kind of company it is. This is exactly the kind of analysis people do when picking individual stocks versus buying an index fund — except here, you’re getting thousands of companies bundled together instead of one. If we base it on that, then VOO is better quality and is more expensive.

Its companies had a 29.4% ROE, as opposed to the 25.6% ROE for the wider mix of VTSAX. VOO’s price-to-earnings ratio (P/E) – a measure of how much you’re paying for every dollar of profit a company earns – is 28.1x, compared with VTSAX’s 27.4x.

VOO’s price-to-book ratio, which is a rough yardstick of valuation compared to the true worth of the business, is 5.5x to VTSAX’s 5.0x. And VOO’s businesses are increasing their profits at a slightly higher rate as well – 23.8% vs. 22.7%. In other words: You’d get a book of companies with around 15% higher ROE at a roughly 2.6% higher price. If terms like growth rate and profit expansion sound unfamiliar, our guide on what growth stocks are and how to calculate a stock’s growth rate breaks it down simply.

That’s not a coincidence. The S&P 500 is a group of large, profitable, and established companies, by design. VTSAX has those same giants, but there are thousands of other small, less-tested businesses included, some of which may be the next big winners, and some that will not.

The size difference is another factor to consider as well. The median company in VOO is worth $474.5 billion. In VTSAX, it’s $340 billion. But neither is small – these are still large companies – it tells you that VOO goes the extra mile to go for the biggest names in the market.

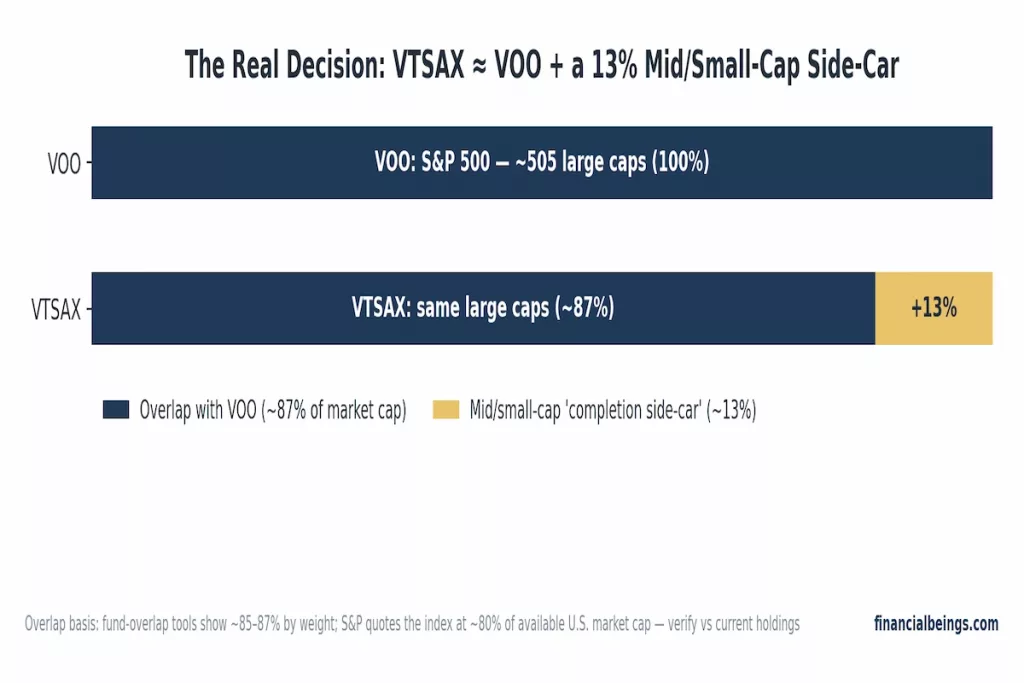

The Real Decision: A 13% Small/Mid-Cap Sidecar

This is indeed the resolution of the VTSAX vs. VOO debate, and it is actually not as difficult as it is thought to be.

87% of the market value of VTSAX is in the same large-cap stocks that you already have in VOO. The entire fund is not an entirely new beast; it’s all of the stock in the S&P 500, plus about 13% more mid-sized and smaller companies that didn’t go into the S&P 500. VTSAX is just like VOO with an extra seat on the side: same engine with a side-car.

The difference is brought out in stark contrast by the number of holdings. VOO owns 505 companies. VTSAX owns 3,484. If diversification, putting your dollars behind more firms, so one can’t sink you, is important to you, VTSAX offers you a lot more of that, though in this instance, it doesn’t as much as one might think boost returns.

One disclaimer, however, and that’s the 87% is far from conclusive. The “Fund-overlap” tools which compare holdings by weight tend to fall somewhere in between at 85% and 87%. Using a different measure, the S&P’s own materials say it’s a measure of about 80% of the value of the U.S. market.

If there are slightly different percentages shown elsewhere, that’s because that’s the takeaway when it comes to the core of VTSAX being a fund of funds versus it being a separate fund.

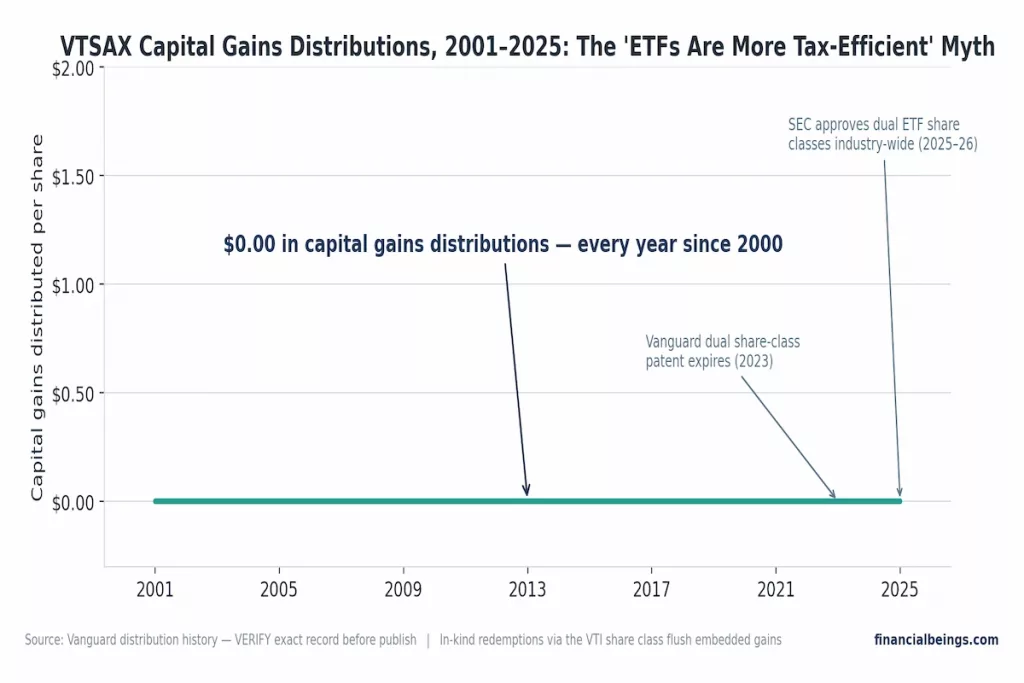

The Tax Question Everyone Gets Wrong

Most of the web is using this comparison the wrong way round.

The old saying goes that ETFs — funds that trade on an exchange like a stock, such as VOO — are more tax-efficient than mutual funds like VTSAX. The logic seems sound: The ETF has a structural feature that ensures it does not generate taxable events within the fund, and it appears that the mutual fund can’t do the same.

If you want the broader picture of how these two investment vehicles differ beyond just this tax question, our Stocks vs ETFs comparison goes into more detail.

However, VTSAX’s actual track record: It has paid out $0 in capital gains distributions each year since 2000, zero. For more than 20 years. It is simply a distribution that a fund must make to satisfy the tax laws upon the sale of an investment that the fund has gained on, but you haven’t sold.

If VTSAX was the tax-inefficient one, you would see at least some of the payouts in your tax bill. You don’t. The answer lies in an aspect of financial “plumbing” that no investor will hear of. There is a twin ETF of VTSAX, called VTI, that has the same portfolio.

With its structure, Vanguard allows for large-scale “in-kind redemptions” by institutions, where Vanguard has cash in the fund and redeems the large institutions in kind (that is, in stock, rather than in cash), thus avoiding a tax trigger. The idea itself is a clever piece of engineering.

The idea itself is a clever piece of engineering — and it ties into the broader structural distinctions covered in our ETF vs ETP breakdown, if you want to understand exactly how these exchange-traded products are built.

Vanguard has had a patent for it to prevent its rivals from replicating the ruse. This patent expired in May 2023. Since then, the SEC has begun to grant exceptions to the rule for other firms, such as Dimensional Fund Advisors in November 2025 and some 30 others, including BlackRock, JPMorgan, Fidelity and State Street, in December 2025.

As of March 2026, the applicant process had been finalized with some 45 of the over 90 applicants being approved. That’s a feature that in the past could only be claimed by Vanguard and is now spreading to a growing list of companies. Interesting but not a factor to consider today.

True Cost of Ownership (Beyond 0.04% vs. 0.03%)

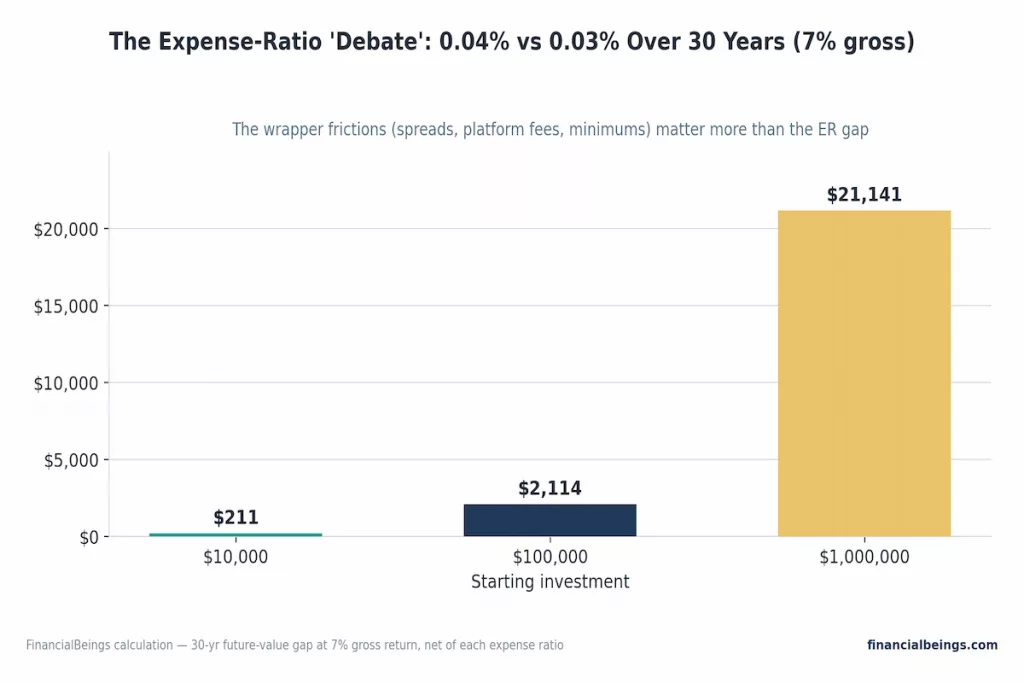

Annual fees expressed as a percentage of your invested money, called the “expense ratio,” is a favorite battleground among investors. VTSAX has an annual fee of 0.04%. VOO charges 0.03%. This one-hundredth of a percent difference is considered true competition in the online world, so let’s actually compare the prices.

The expense ratio difference costs you about $211 for 30 years of investment on $10,000 invested at 7% with a gross return. On $100,000, it’s $2,114. On $1,000,000, it’s $21,141. For most people reading this with a normal-sized account, we’re talking about a couple hundred dollars over 30 years – which is just a nice dinner out.

But here’s the part of Reddit nobody ever gets into a debate about that is more important: the disagreements within each fund. Unlike ETFs, VTSAX (a mutual fund) does not have a bid/ask spread, or the thin margin between what it offers and what it asks, and the trades occur at the official price, or NAV, without any time lag. V

OO does have a spread – usually about 0.01%, but it can be a few basis points up or down from its value; most recently, it was -0.02%. Most of the time, VTSAX trades commission-free, but you may have to pay a transaction fee if you buy it through a broker such as Fidelity or Schwab ($75 at Fidelity and $74.95 at Schwab).

Conversely, VTSAX has native support for auto-investing the dollar amount, while the availability of fractional-share investing with VOO will depend on your brokerage provider.

All these rubrics are inconsequential in isolation. When taken together, however, their significance is greater than the attention they receive in the “debate” over the expense ratio.

Which Should You Choose?

If you are looking for the easiest possible solution, with no thinking required, just one fund, then either VOO or VTSAX is sufficient. If you want to compare VOO against a growth-focused option instead, our SCHG vs VOO breakdown covers that angle too.

Either one is a heck of a good bet. If you want to own more of the market, and the smaller companies with the potential to be tomorrow’s giants, VTSAX’s built-in tilt does just that. If you prefer to focus on the big, well-established U.S. stocks and aren’t concerned with the smaller names, then VOO is the safer choice.

Some investors opt to own both, or even a separate fund for smaller companies in addition to VOO; it’s sort of like re-creating VTSAX’s mix, but with finer control over the proportion. Type of account is also a factor.

Because growth inside a Roth IRA is tax-free, tax efficiency is a non-issue — simply choose the fund that is the best fit for their minimum investment and auto-invest options. VTSAX’s clean capital-gains history is another edge in a regular (taxable) account, particularly if the industry-wide transition to tax efficiency of the VOO approach hasn’t been fully embraced yet.

Frequently Asked Questions

Is VTSAX better than VOO?

Not necessarily; it depends on what you want. VTSAX has been slightly behind VOO for the last 5 and 10 years, but ahead for the last year. VTSAX also provides thousands more businesses. There is no clear definition of which is better; they serve slightly different purposes and have the same general approach.

Is VTSAX better than S&P 500?

VTSAX contains companies from the S&P 500, as well as smaller companies, which means performance will be driven by how the smaller companies do in comparison to the S&P. The S&P 500 (VOO) had a slight edge over VTSAX over the last 10 years, but the last year was a better time to be in VTSAX.

Is VOO more tax-efficient than VTSAX?

In fact, since 2000, VTSAX has not paid a capital gain. It is structured this way because embedded gains can be extracted from the ETF’s twin, VTI. The notion that ETFs are always more tax-efficient is a popular one that isn’t supported by VTSAX’s record.

What is the 10-year return on VTSAX?

As of June 30, 2026, VTSAX’s official 10-year annualized return is 15.03%. During all that time, VOO gained 15.47% annualized — a modest gap, but one that compounds the longer investors hold.

Does Warren Buffett still own VOO?

Berkshire Hathaway’s holdings of funds have varied over time, and holdings may change from quarter to quarter as disclosed. Instead of making an assumption, see Berkshire’s latest 13F submission to the SEC for what they actually own.

Can I convert VTSAX to ETF without paying taxes?

As a tax-free conversion, Vanguard offers a way for shareholders of VTSAX to exchange into its Vanguard Twin, VTI, because it’s considered an exchange, not a sale. This option is only available in paired mutual funds and ETF share classes with Vanguard.

Should I hold both VTSAX and VOO?

You can, but the vast majority of your holdings are already in VTSAX, so having both is nearly the same exposure with a double expense ratio. You can simply choose VTSAX for the broad market or VOO just for the large-cap market.

References

- Vanguard. Vanguard Total Stock Market Index Fund Admiral Shares (VTSAX) — Fund Profile, data pulled 8 July 2026. View Source

- Vanguard. Vanguard S&P 500 ETF (VOO) — Fund Profile, data pulled 8 July 2026. View Source

- Google. SERP for ‘vtsax vs voo’ including People Also Ask box, accessed 8 July 2026. View Source

- Bing. SERP for ‘vtsax vs voo’ including Copilot answer, accessed 8 July 2026. View Source

- Dimensional. Newsroom — Dimensional Receives SEC Approval for ETF Share Classes, November 2025. View Source

- Bloomberg. SEC Permits BlackRock, JPMorgan to Offer Dual-Share-Class Funds, 17 December 2025. View Source

- Pensions & Investments. SEC Approves Dozens of ETF Share Class Filings. View Source

- etf.com. Buffett’s Berkshire Sold SPY & VOO Holdings in Q4 2024. View Source

- Sound Mind Investing. Schwab Increases Transaction Fees for Vanguard and Fidelity Funds. View Source

- University of Chicago Business Law Review. Unplugging Heartbeat Trades & Reforming the Taxation of ETFs. View Source

- White Coat Investor. VTSAX vs. VTI — Dual Share Class Mechanics. View Source

- Yahoo Finance. VTSAX vs. VOO, April 2026. View Source