AI stocks are companies that have been helped by technologies such as machine learning, automation, and cloud computing. The importance in 2026 is due to AI gaining momentum in all industries, and these stocks are among the most appealing long-term investments.

The most promising AI stocks 2026 will be those that have high financial growth, an increase in profitability, and cash flow generation. Apple, Amazon, NVIDIA, Microsoft, and others have consistently grown in revenue, margin, and free cash flow, which makes them significant in artificial intelligence investing in the future.

So, in this guide, we will walk you through the best AI stocks to buy in 2026, helping you identify high-growth opportunities, evaluate financial strength, and make smarter long-term investment decisions.

Why AI Stocks Are Booming in 2026

AI stocks 2026 are becoming popular because companies are reporting good growth in revenues, great margins and high cash flows as artificial intelligence is integrated into the business operations. Such technologies like chatbots, automation, and cloud computing are currently extensively implemented in real life and assist companies in enhancing their efficiency and scaling at a higher rate.

The use of AI is evident in streaming, e-commerce, and enterprise software, which utilize machine learning–powered platforms like Adobe Stock. For example, Netflix (recommendation systems), the work of Tesla (automation), and cloud-based AI applications of Microsoft demonstrate the extent of the integration of AI into everyday practice. This rising use is manifested in financial activities, as such companies as Amazon expanded their revenue by 513,983M to 716,924M, and Alphabet by 282,836M to 402,836M, thus indicating the growing demand in AI-based services.

This boom is also fueled by corporate investment in AI. Businesses are increasing profitability and growth. NVIDIA’s operating margin expanded from 20.68% in 2023 to 60.38% in 2026, while Meta’s operating margin increased from 24.82% in 2022 to 41.44% in 2025. Meanwhile, good cash flow generation, in the case of Apple, 98,767M and Microsoft, 71,611M in 2025 free cash flows, is a sign of financial health.

How We Selected the Best AI Stocks

We determined the most suitable AI stocks 2026 by revenue growth, profitability, and the strength of cash flows of individual companies, as well as their contribution to artificial intelligence.

- First, Companies such as Amazon, Microsoft, and Alphabet have positive upward trends, which are indicative of a growing demand for AI-based services such as cloud services and automation. This will make sure that real business activity supports growth.

- Second, market leadership and participation in the AI area are significant. The companies chosen are major participants in such spheres as AI chips, cloud platforms, and data-driven systems.

- Companies with improving margins and strong free cash flow, such as Micron and Broadcom, often demonstrate solid financial strength. In addition, their long-term growth trends suggest these stocks could remain attractive AI investment opportunities for long-term investors.

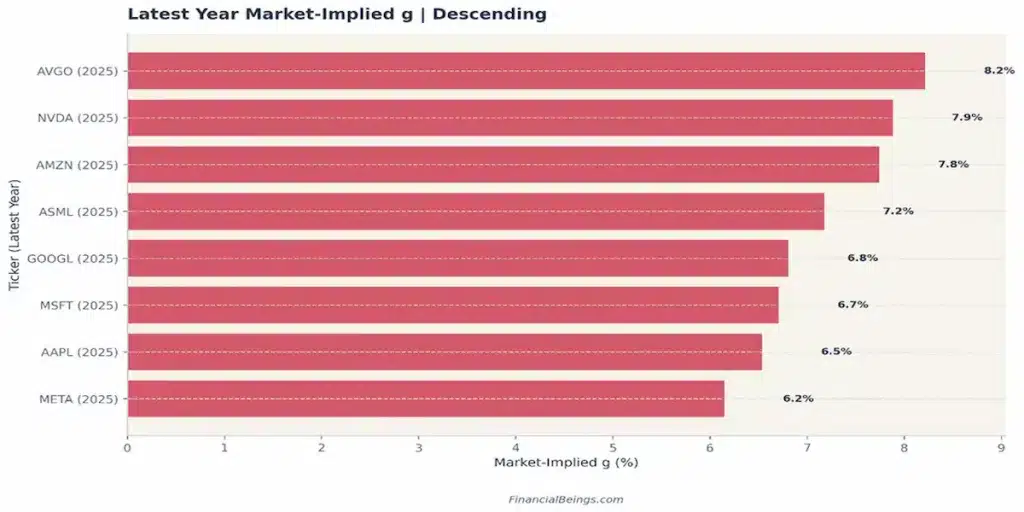

Figure 1: Market-Implied Growth Rates (g) for Leading AI Stocks (2025)

Broadcom (8.2%), NVIDIA (7.9%), and Amazon (7.8%) have the greatest expected growth, indicating high future potential among AI stocks.

Top AI Stocks to Buy in 2026

Here are the Top AI Stocks to Buy in 2026, including Microsoft, Nvidia, and other high-growth AI leaders.

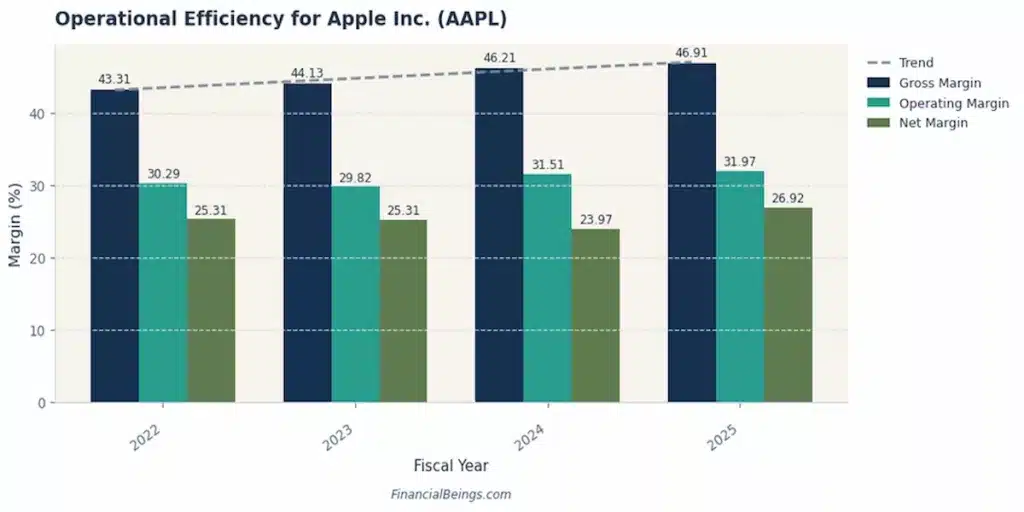

Apple Inc. (AAPL)

Apple Inc. (AAPL) Financial Performance and Operational Efficiency (2022–2025)

Apple is a leading American multinational technology company its headquartered in Cupertino & California. It is globally famous for designing, manufacturing & marketing premium consumer electronics – software & online services, especially the iPhone, Mac & iPad.

The company has built a strong ecosystem that gives it a significant long-term advantage in personalized on-device artificial intelligence. However, its heavy reliance on iPhone sales remains a key risk compared to cloud-focused competitors.

Key Financial Snapshot:

- Revenue (FY2022): $394.33 billion

- Revenue (FY2025): $416.16 billion

- Net Profit Margin: 26.92%

- Free Cash Flow: $98.77 billion

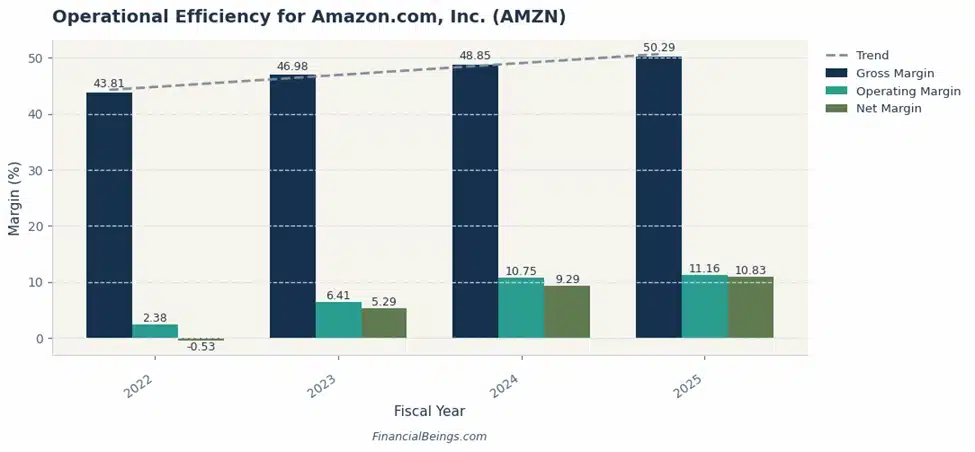

Amazon.com Inc. (AMZN)

Amazon (AMZN) Revenue Growth and Margin Improvement (2022–2025)

Amazon has been leading AI firms since it utilises artificial intelligence in e-commerce, logistics and cloud computing. Amazon is the biggest online retailer and a significant tech firm in the world that was established by Jeff Bezos in 1994 as an online bookstore.

The main offerings are Amazon Marketplace, Amazon Prime, and Amazon Web Services (AWS), with AI working in the recommendation systems, warehouse automation, and cloud-based machine learning. One of the risks is the relatively low net margins compared with peers, which may be driven by high operational costs and reinvestment policies. If you want a deeper investment analysis, read this detailed Amazon stock review.

Financial Highlights:

- Revenue: $716.9 billion

- EBITDA: $165.3 billion

- Free Cash Flow: $7.7 billion

- Net Margin: 10.83%

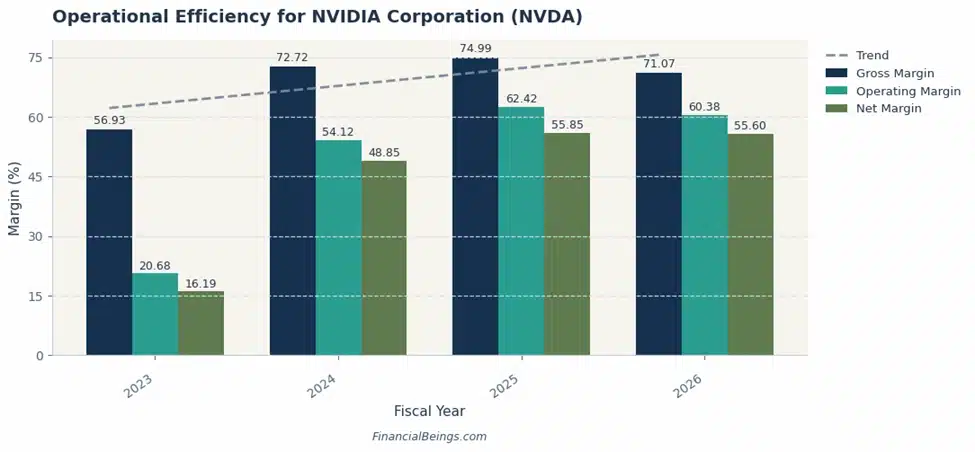

NVIDIA Corporation (NVDA)

NVIDIA (NVDA) AI-Driven Growth and Margin Expansion (2023–2026)

NVIDIA is the leading AI company because it is a worldwide pioneer in accelerated computing and artificial intelligence. NVIDIA is an American technology company that started as a producer of graphics processing units (GPUs) to be used in gaming, but today drives the core of modern AI, data centres, and autonomous systems.

Its GPUs play a crucial role in training AI models, which makes it a fundamental infrastructure provider in the AI community. The primary risk is that the company relies heavily on AI demand cycles, and a decrease in the growth of the industry will affect the performance.

Key Financial Metrics:

- Revenue: $215.9 billion

- EBITDA: $144.6 billion

- Free Cash Flow: $96.7 billion

- Net Margin: 55.60%

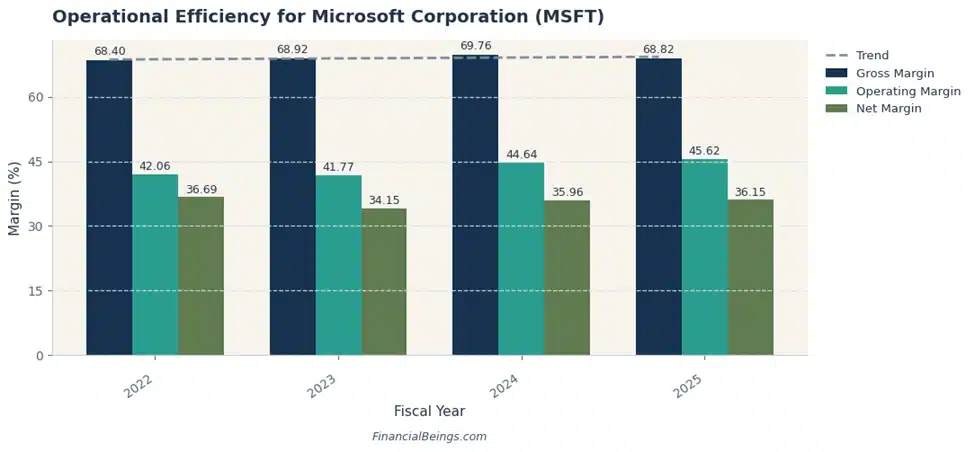

Microsoft Corporation (MSFT)

Microsoft (MSFT) Financial Growth and Profitability Trends (2022–2025)

Microsoft is leading the AI companies since it incorporates artificial intelligence in cloud computing, enterprise software, and productivity tools. Microsoft Corporation is a leading American multinational technology company founded in 1975 by Bill Gates and Paul Allen.

Its headquartered in Redmond, Washington & it is the biggest software seller in the world that provides products such as Windows, Microsoft 365, Azure cloud service, Xbox, and artificial intelligence development. The most significant risk is the rise in the intensity of competition in cloud and AI services, which can strain the margins long-term.

Financial Performance:

- Revenue: $281.7 billion

- EBITDA: $160.2 billion

- Free Cash Flow: $71.6 billion

- Net Margin: 36.15%

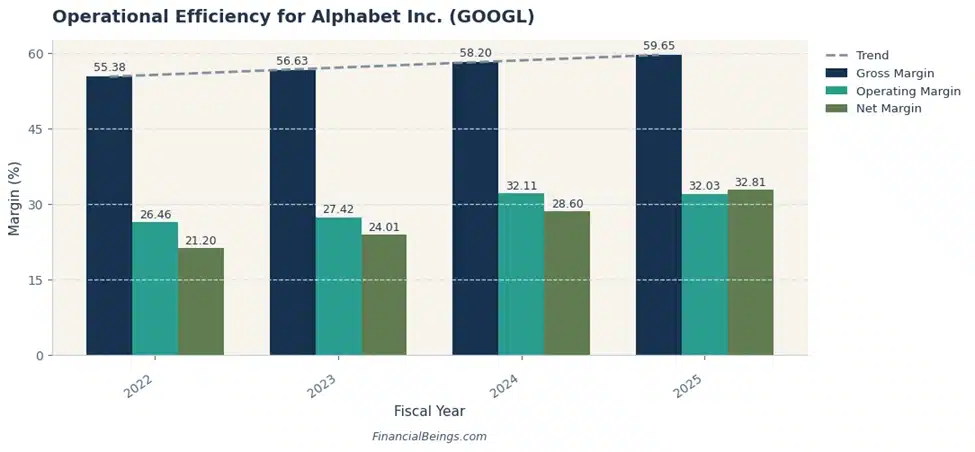

Alphabet Inc. (GOOGL)

Alphabet (GOOGL) Revenue, Cash Flow, and Margin Trends (2022–2025)

Alphabet is leading AI companies because it implements artificial intelligence on search, advertising, and cloud computing platforms. Alphabet Inc. is a multinational holding corporation that was established in 2015 as the mother company of Google, YouTube, Android, and other subsidiaries, including Waymo and Verily.

It was developed to enhance operational focus, which enables Google to focus on the core internet services as it ventures into AI and advanced technologies. One major risk is its heavy dependence on advertising revenue, which can be affected by market conditions and regulatory constraints.

Key Financial Indicators:

- Revenue: $402.8 billion

- EBITDA: $180.7 billion

- Free Cash Flow: $73.3 billion

- Net Margin: 32.81%

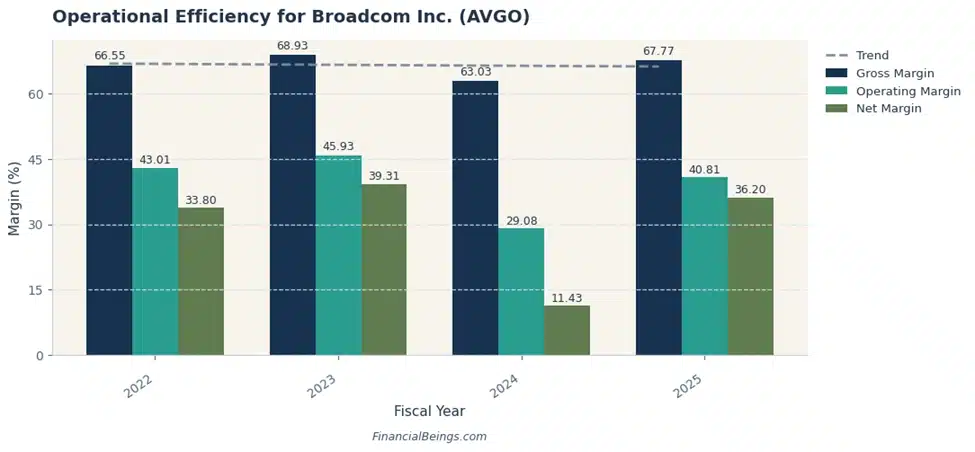

Broadcom Inc. (AVGO)

Broadcom (AVGO) Profitability and Cash Flow Performance (2022–2025)

Broadcom is leading the top AI firms because it offers semiconductor and infrastructure software solutions to support artificial intelligence systems. Broadcom Inc. is a technological powerhouse with its headquarters in Palo Alto, California, that designs and supplies a variety of semiconductor and software products.

It provides data centres, networking, wireless, and storage markets, the technology of which constitutes a fundamental backbone of digital infrastructure. Its dependence on the large enterprise clients and acquisitions is a major risk, as it could influence the stability of an issue in the integration.

Financial Highlights:

- Revenue: $63.9 billion

- EBITDA: $34.7 billion

- Free Cash Flow: $26.9 billion

- Net Margin: 36.20%

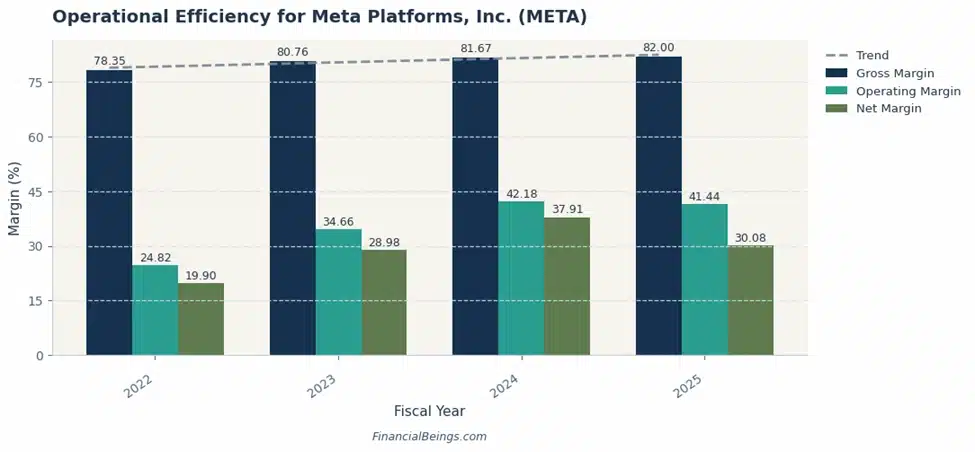

Meta Platforms Inc. (META)

Meta (META) Efficiency Improvements and Margin Expansion (2022–2025)

Meta is leading the top AI companies because it applies artificial intelligence to maximise social media networks, advertising systems, and content suggestions. Meta (previously Facebook, Inc.) is a multinational technology firm founded by Mark Zuckerberg and runs operating platforms, including Facebook, Instagram, WhatsApp, and Threads.

The company has since been working on building into the metaverse and further developing AI technologies within its digital ecosystem since rebranding in 2021. The biggest risk is that it relies on advertising income, which is unstable and has the potential to change due to market dynamics.

Key Financial Snapshot:

- Revenue: $201.0 billion

- EBITDA: $105.7 billion

- Free Cash Flow: $46.1 billion

- Net Margin: 30.08%

ASML Holding N.V. (ASML)

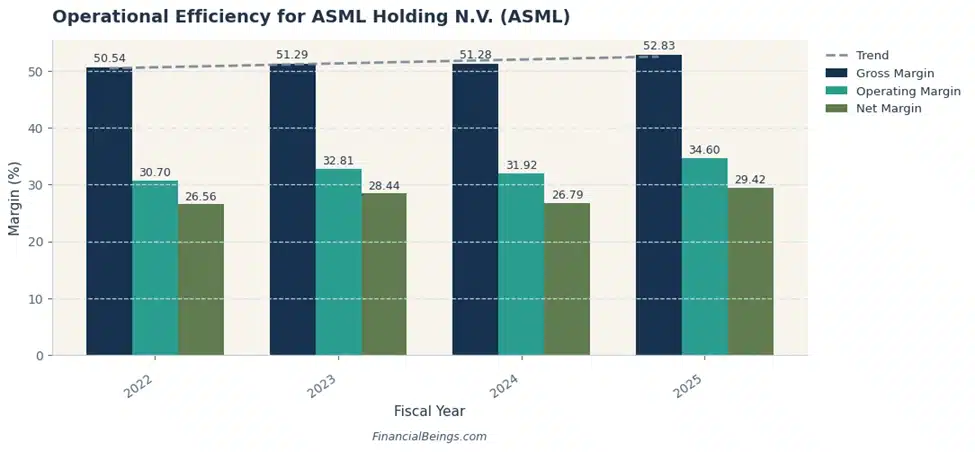

ASML Financial Performance and Semiconductor Market Strength (2022–2025)

ASML is leading AI company because it offers superior semiconductor equipment that is utilised to produce AI chips. ASML Holding N. V. is a Dutch multinational corporation headquartered in Veldhoven, Netherlands and the largest manufacturer of photolithography systems in the world.

It is the sole company that manufactures extreme ultraviolet (EUV) lithography equipment, which is needed to make sophisticated microchips used in artificial intelligence. Risk is the political uncertainty and reliance on supply chains, which can impact operations and international demand. For better understanding, you may explore this article on ASML stock intrinsic value analysis.

Key Financial Highlights:

- Revenue: $32.7 billion

- EBITDA: $12.6 billion

- Free Cash Flow: $11.0 billion

- Net Margin: 29.42%

Financial Comparison of Top AI Stocks

| Company | Revenue ($M) | EBITDA ($M) | Free Cash Flow ($M) | Net Margin (%) |

| Apple | 416,161 | 144,748 | 98,767 | 26.92 |

| Amazon | 716,924 | 165,341 | 7,695 | 10.83 |

| NVIDIA | 215,938 | 144,552 | 96,676 | 55.60 |

| Microsoft | 281,724 | 160,165 | 71,611 | 36.15 |

| Alphabet | 402,836 | 180,698 | 73,266 | 32.81 |

| Broadcom | 63,887 | 34,714 | 26,914 | 36.20 |

| Meta | 200,966 | 105,713 | 46,109 | 30.08 |

| ASML | 32,667 | 12,550 | 11,027 | 29.42 |

Best AI Stocks for Beginners

Beginners should consider AI stocks that showed steady growth in revenues, high cash flow, the lowest market implied growth and high profitability, as these minimise the risk and provide exposure to artificial intelligence.

Good starting points would be companies such as Apple, Microsoft, and Alphabet, since they demonstrate a stable financial performance. In 2025, Apple generated 98,767M in free cash flow, and Microsoft and Alphabet generated 71,611M and 73,264M, respectively. These strong cash flows are good signs of financial stability, and such is valuable to beginners who require lower-risk investments. Moreover, these companies are spread over various segments such as cloud computing and digital platforms, making them less risky.

To achieve balanced growth, Amazon and Broadcom are also worth considering for beginners. Amazon has a high growth in revenues, whereas Broadcom has a high profitability with a net margin of 36.20%. These stocks are a good combination of growth and stability, and hence an ideal starting point for AI investing.

Risks of Investing in AI Stocks in 2026

AI stocks 2026 come with risks such as high valuation, market buzz and rising competition that investors should consider before investing.

Overvaluation

The growth in revenue and margins of many AI stocks is strong, which may result in high expectations. For example, companies such as NVIDIA and Broadcom are experiencing high profitability and growth rates, which can lead to higher prices in comparison with their financial performance. In case the growth decreases, stock prices can re-adjust.

Market Hype

AI is one of the most discussed sectors, and speculative investors can be drawn to it. This hype has the potential of creating short-term changes in price despite the strong company fundamentals. There is a risk of investors purchasing according to trends, not actual financial information.

Competition

The AI sector is extremely competitive, with such companies as Microsoft, Alphabet, Amazon, and Meta investing significant funds. With the escalation in competition, it could decrease profit margins and reduce the growth of certain companies over time.

AI Investment Strategy for 2026

A smart AI investment plan in 2026 is based on long-term development, diversification of good firms and entering at the right time, not at the hype of the market.

Long-Term vs Short-Term

Long-term investing is more appropriate for AI stocks, as most companies continue to increase their technologies and sources of revenue. The revenue and cash flow of companies such as Microsoft, Alphabet, and Amazon are steadily increasing, which is why it is possible to occupy these positions in the long run. Market sentiment and news can make prices volatile, and thus, short-term trading can be risky. Compounding growth and bettering margins are advantageous to long-term investors. For investors seeking diversified opportunities outside pure AI plays, these best long-term growth stocks to buy may also be worth considering.

Diversification

Investors are advised to diversify their investments across different types of AI companies. For instance, combining platform companies such as Apple and Alphabet with infrastructure players like NVIDIA, ASML, and Broadcom can help reduce risk. Many investors comparing NVIDIA vs Google stock opportunities often look for exposure to different parts of the AI ecosystem, including cloud computing, semiconductors, and digital services, which can help balance portfolio performance.

When to Buy

An ideal investment is one in which companies perform well financially but market expectations are not too high. Stocks with predictable cash flows, such as Apple and Microsoft, may be a safer entry point; more growth companies may be added over time to capture further upside. For better diversification, investors often combine high-growth AI stocks with income-generating assets such as dividend stocks to create a more balanced portfolio.

Common Mistakes to Avoid When Buying AI Stocks

Hyping, lack of research, and Panic selling are some of the common mistakes that investors should avoid because they contribute to poor investment decisions in AI stocks.

Following Hype

AI stocks are purchased by many investors simply because they are trending. The growth of companies such as NVIDIA and Amazon can make them interesting to purchase, but it is possible to lose money if you overstate their financial performance.

No Research

The risk of overlooking data is a major mistake. Among the most important indicators that should be paid attention to by investors are revenue growth, margins, and cash flow. The financial strength of companies such as Apple and Microsoft stocks are stable, and this is significant in making informed decisions.

Panic Selling

There may be short-run volatility in AI stocks. When the market declines, selling at a low point may lead to losses, particularly when the long-term growth is good. It is important to keep track of the financial performance to prevent emotional decision-making on the part of investors.

Frequently Asked Questions (FAQ)

Are AI stocks a good investment in 2026?

Yes, AI stocks can be considered a good growth area in 2026 due to the increase in revenues and profitability of leading firms. For instance, NVIDIA’s revenue was 215,938M with an operating margin of 60.38%, whereas Amazon expanded to 716,924M. Financial stability is also indicated by strong cash flows by such companies as Apple (98,767M) and Alphabet (73,266M).

Which AI stock has the highest growth potential?

Depending on risk tolerance, the “highest” growth potential in AI can be found in the various stocks that provide exposure to infrastructure, software, or specialised hardware. NVIDIA (NVDA) is still a pillar of AI infrastructure. Its operating margin has risen in 2023 and 2026, increasing to 20.68% to 60.38%, respectively, and other firms such as Broadcom (AVGO) are popular with custom AI accelerators and high-bandwidth memory (HBM).

Is NVIDIA still a good buy?

NVIDIA is also a good choice as it is highly profitable and growing. The company produced 96,676M of free cash flow, and it exhibits excellent margin growth, which indicates efficient performance. Nevertheless, investors should consider volatility possibilities, which may occur because of elevated growth projections. For a deeper valuation and growth analysis, check this guide on Is NVIDIA a good stock to buy now?.

Can beginners invest in AI stocks?

Yes, beginners can invest in AI shares by using exchange-traded funds (ETFs), which pack several different AI-related businesses into a single investment. By doing so, you can have exposure to the top chipmakers and software innovators without having to do any research on individual stocks.

Final Thoughts

AI stocks in 2026 have been among the most promising investment opportunities, as the revenues, profitability, and cash flows of leading companies have grown rapidly. The financial information reveals that companies such as NVIDIA, Amazon, Apple, and Alphabet are growing, and their margins and efficiency remain strong.

The most crucial thing for investors is to invest in companies with steady long-term performance rather than short-term hype. By investing in stable stocks alongside high-growth AI leaders, investors can enjoy the continued growth of artificial intelligence technologies while mitigating risks.