You’ll have two conflicting fears when weighing between Microsoft and Adobe: that you’re paying too much for the safe giant & that you’re getting a falling knife by buying the cheap one.

Adobe has dropped to approximately $204, down from about $350 a few months ago, for those who purchased the stock. Microsoft sits at around $390.74, a $2.9 trillion colossus that trades well below its 52-week high after sliding roughly 17% year-to-date. It’s an elite business on both sides.

Everything comes down to the price you’re going to pay for what you’re going to get. Here are the key Microsoft vs. Adobe stock differences to consider before making a decision.

Microsoft vs. Adobe Stock Comparison at a Glance

We’ll begin by giving you a mini snapshot of both companies’ current positions.

| Metric | Microsoft (MSFT) | Adobe (ADBE) |

| Market cap | ~$2.9 trillion | ~$82 billion |

| Share price | $390.74 | $204.02 |

| Revenue (FY2025) | $281.7B | $23.8B |

| Revenue growth (YoY) | +15% | +11% |

| Free cash flow (TTM) | $85.7B | $9.9B |

| P/E (trailing / forward) | 23.3× / 20.2× | 11.7× / 7.5× |

| Gross margin | 68% | 89% |

| Dividend | $3.64/yr · ~0.9% · 21-yr grower | None · $25B buyback |

| AI exposure | Copilot + Azure; 60%+ Fortune 500 | Firefly; 70M+ users, $400M AI rev |

Microsoft is more than 35 times larger than Adobe, and pays you a dividend to wait. With Adobe, you buy similar profits at roughly half the earnings multiple — but you are buying a far smaller company. Same industry, very different deals.

Microsoft Business Overview

When it comes to a utility for the business world, Microsoft comes closest: Hundreds of millions of workers open its software every morning, and their employers pay the bill, like clockwork. During FY25, the revenue was reported to be around USD 282 billion across three engines: Productivity (Office 365, Teams, LinkedIn); Intelligent Cloud (Azure); More Personal Computing (Windows, gaming).

The financial pillars are quite strong for this size: operating margin of around 47%, net margin of about 39% and a strong balance sheet with about $34 billion in net cash.

Microsoft has also increased its dividend consistently over the past 21 years, and thus, it is a good income stock for patient investors. Now imagine you had to explain Microsoft to a 12-year-old, and it was the electricity company the office uses, and there are a lot of people who pay it every month without any problem.

Adobe Business Overview

The world’s designers, photographers and marketers open their inboxes every morning to find the tools that Adobe has created. The FY25 revenue was roughly in the ballpark of $24B and was generated through three different areas: Creative Cloud (Photoshop, Illustrator, Premiere Pro), Document Cloud (Acrobat), and Experience Cloud (marketing software).

The economics of Adobe are what’s amazing. When you have a gross margin of 89%, that’s software-royalty territory; all those dollars of revenue cost you very little. Return on equity is in the neighbourhood of 48%, and return on operating assets is in the neighbourhood of 58%.

The company does not pay a dividend, but has approved a fresh buyback program of up to $25 billion through 2030, opting to buy back shares instead of paying out cash.

Revenue Growth Comparison

In one year, Microsoft has earned more than Adobe does all year. In FY25, revenue surged by 15%, to $282 billion, adding approximately $37 billion in sales in just one calendar year, over 1.5 times what Adobe generated in total for the entire year. Adobe was up 11 per cent to $23.8 billion, though its growth was not as impressive.

The shocking number in the numbers: Residual profit, the number that matters to a value investor, increased faster at Adobe last year, rising 31% compared to Microsoft’s 19%. Growth is not necessarily synonymous with good investment. The next section explains why exactly!

Profitability Comparison

The two operators are top-notch. But they are the best at different things, and it’s important to know the difference.

| Profitability (FY2025 / TTM) | Microsoft | Adobe |

| Gross margin | 68% | 89% |

| Operating margin | 47% | 37% |

| Net margin | 39% | 30% |

| Return on equity | 30% | 48% |

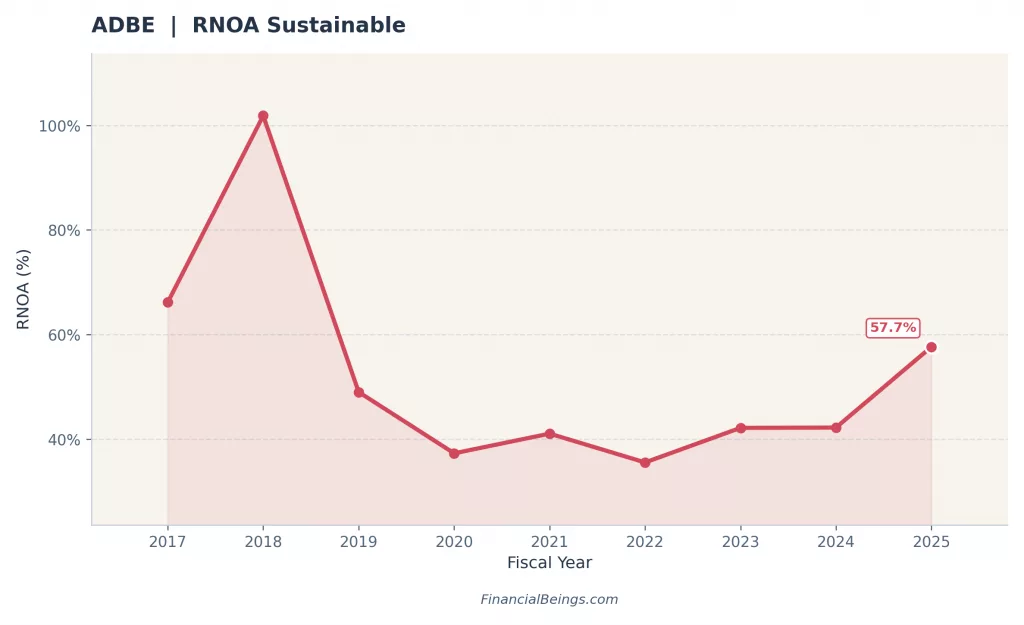

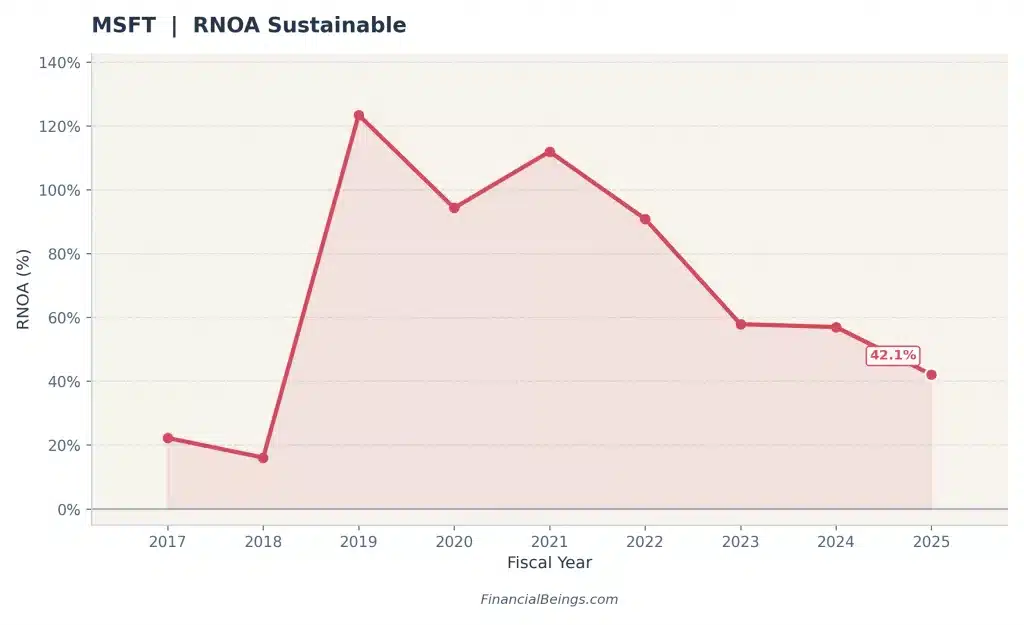

| Return on operating assets (RNOA) | 42% | 58% |

| Asset-turnover trend | Falling (4.1× → 1.1×) | Rising (≈1.3× → 1.9×) |

The part most headlines fail to mention: As Microsoft’s massive AI investment slows down, the returns on every dollar invested have been decreasing, from triple digits back in 2019 to approximately 42% today. Adobe is getting better and requires less hardware.

Microsoft’s operating and net margins are its strengths. Adobe is doing better on the gross margin, ROE and ROA on its actual asset base. It’s not the trajectory, but rather which number looks better today.

Financial Beings Valuation Lens

This is the crux of the article. Imagine a share price as a bet about the future. The core challenge of every price is the assumption of a rate of growth which must be maintained forever to justify the price today.

| Growth (%) | ADBE Value ($B) | ADBE Value % | MSFT Value ($B) | MSFT Value % |

|---|

Model Value % > 100% = The model value exceeds the current market cap under the stated assumptions. Model Value % < 100% = The current market cap is above the model value under the stated assumptions. Model Value % = 100% = The model value matches the current market cap at the assumed growth rate.

At 5% growth, ADBE’s model value already reaches 156% of its current market cap while MSFT reaches only 68%. At 8% growth, ADBE reaches 369% while MSFT reaches 152% — the same growth assumption produces very different verdicts on the two stocks.

The market-implied breakeven growth rates diverge sharply: ~1.7% for ADBE versus ~6.8% for MSFT. The market is asking Microsoft’s cloud (Azure), productivity (Microsoft 365 / Copilot) and intelligent-cloud franchises to compound at nearly 7% in perpetuity to justify a $2,903B market cap, while Adobe’s Digital Media (Creative Cloud, Document Cloud) and Digital Experience businesses need under 2% to justify $82B.

Note: Under the 10% hurdle rate scenario set, ADBE sits above 100% Model Value across the entire tested 2%-9% range — its breakeven of ~1.7% lies just below the tested floor, so even a near-stagnant growth path clears the bar. MSFT crosses 100% Model Value at ~6.8% growth, inside the tested range, climbing to 292% at 9% growth.

According to our valuation work, performed at a 10% required return, the result is nothing short of eye-catching:

| At a 10% required return | Microsoft | Adobe |

| Growth the price already assumes | ~6.8% | ~1.7% |

| Fair value reached at… | ~7% growth forever | ~2% growth forever |

| Share of price that is "future growth" | ~60% | ~17% |

| Value-to-price at 5% growth | 68% (overpriced) | 156% (cheap) |

The company expects to see a 2% annual growth rate in the price of Adobe. Microsoft's price is betting that there will be no end to its growth rate of approximately 7 per cent per year. Consider which is the more likely wager to succeed. If you want to learn more about growth rates, I recommend checking out our guides on what growth stocks are and how to calculate a stock's growth rate.

As long as it's above 2% growth, it's a dollar for a dollar for Adobe. The business has to achieve about 7% perpetual growth for the business to justify its price to Microsoft in the first place, which is a very steep price to pay over the decades.

Adobe (ADBE) — current price $204.02

| Long-term growth (g) | Intrinsic value / share | Value-to-Price |

| 2% | $210 | 103% |

| 3% | $236 | 115% |

| 4% | $270 | 132% |

| 5% | $318 | 156% |

| 6% | $391 | 192% |

| 7% | $511 | 251% |

| 8% | $753 | 369% |

Green value-to-price = intrinsic value exceeds the market price. Adobe is green in every scenario, including the most conservative.

For the full model behind these numbers, read our Adobe intrinsic value and expected return analysis.

Microsoft (MSFT) — current price $390.74

| Long-term growth (g) | Intrinsic value / share | Value-to-Price |

| 2% | $183 | 47% |

| 3% | $202 | 52% |

| 4% | $229 | 58% |

| 5% | $265 | 68% |

| 6% | $320 | 82% |

| 7% | $411 | 105% |

| 8% | $593 | 152% |

Microsoft stays red (price above value) until growth exceeds ~7%. It only earns a discount in the top two rows.

See the complete model in our Microsoft expected return analysis for 2026–2030.

This is also the case with the traditional multiples. Adobe trades at 11.7× trailing earnings and just 7.5× forward earnings. Microsoft's trailing and forward multiples are 23.3× and 20.2×, respectively. The ratio of PEG for Adobe is 0.58, and for Microsoft is 1.2. On all earnings and cash-based multiples, Adobe is on the lower end.

AI Growth Potential

Microsoft's AI Strategy

AI, for Microsoft, is a relatively new product to sell, and they're doing so on a large scale. Copilot is integrated throughout Office 365, Windows, and Teams, and nearly 70% of the Fortune 500 are already utilizing Copilot, albeit in various capacities. Azure OpenAI is enabling enterprises to deploy their own AI workloads on Microsoft infrastructure, while feeding cloud growth.

The plan is a flywheel sell AI as an add-on for software customers already paying for software, adding to their lock-in and switching costs. The capex of building this flywheel is huge, which is why ROIC is becoming lower, but at the same time, the moat is likely to be increasing.

Adobe's AI Strategy

For Adobe, AI is both its biggest opportunity and its biggest threat. On the opportunity side, Firefly generative AI is integrated into the tools of the Creative Cloud with more than 70 million monthly active users on the freemium AI features, and the company reports about $400 million in direct AI revenue to-date.

Conversely, the threat side is morphing quickly as well, with OpenAI and Google's generative image and video models, as well as Midjourney's generative design, gaining in sophistication. The worry in the market, as evidenced by the decline in the stock price, from ~$350 to ~$204, is that outside models could make creative tools commonplace and destroy the subscription pricing that Adobe relies on. Legal and IP issues related to the training of AI further increase the fog surrounding the issue.

Bull vs Bear Case

Where trust is concerned, the first thing to show is the risk. These are the best arguments for and against.

Adobe: Bear: Growth is slowing. The stock is down from ~$350 already, and cheapness will remain so if the moat actually breaks. If residual profit slowed again for a third successive year, it would be a reflection of the market's negative expectations, not that its expectations were wrong.

Adobe: Bull: Only ~2% growth on about 12x earnings. An 89% gross margin and $9.9 billion of free cash flow are not indicative of a broken business. The balance sheet is rock-solid. Return on capital is not falling, but is recovering. If growth merely reaches the mid-single digits, the upside is significant.

Microsoft: Bear: Sold for ~7% growth forever with about 60% of the quote on a future that hasn't yet been won. The ROE has slowed its pace of growth. At present prices, the margin of safety is limited by buying a great franchise at full price and hoping it remains great for a long time.

Microsoft: Bull: The most lasting brand in technology. Copilot and Azure AI form a flywheel effect that strengthens the 'moat'. Incentives for any patient investors are derived from its 21-year dividend growth streak and fortress balance sheet. In the past, momentum has proven to be a winner even when the valuation was overstretched.

The reason for the low price of Adobe is the market's fear of AI. Microsoft is pricey in the market because there is no doubt. Those are the only two sentences that contain the whole debate.

Which Stock Is Better for Investors?

Well, the truth is, it depends on you.

Among value investors who want to buy things at a margin of safety, Adobe is the better choice, as it carries only 2% expectations of growth, and 83% of the quote is based on a business already in existence. It's a real risk (AI disruption), and a real discount as well.

If you prefer income and stability, you'd be a better investor in Microsoft. More diversified, more predictable, a rising dividend and a type of franchise that doesn't come with a surprise when it comes to the downside. It's a premium product, and it will give you premium-grade durability.

The clear framing: Microsoft is the better business. Adobe is the better price. The answer depends on whether you prefer to sleep well or to spend cheaply.

Final Verdict

A value investor today has to choose between Adobe and Microsoft, and for those who think that the fear of being disrupted by AI is exaggerated, the Adobe stock is the superior value. The logic is straightforward: a price that reflects only marginal growth, enough to provide a nice margin of return, but not enough to justify the risk of the price collapsing further, a good return on capital, and a clean balance sheet. The risk is just as evident: If generative AI is truly a destroyer of the moat, then the cheap price is deserved.

To most investors, Microsoft is the safer play and better business. It's also priced for excellence; about 60% of today's quote is based on perpetual growth, which has yet to arrive. That's not a reason to avoid it; it's a reason not to call it cheap.

For a standalone verdict on the giant, see whether MSFT stock is a buy at today’s price.

The safe play is Microsoft. The maths is cheaper at Adobe. And the maths is what value investing rewards.

This is not a financial recommendation; it's only an analysis. It all comes down to your opinion of the value of Adobe's competitive moat as well as your own tolerance for risk.

Is Microsoft better than Adobe stock?

Overall, Microsoft is regarded as a superior stock picking choice because of its strong diversification between cloud computing (Azure), enterprise software and AI monetization. Adobe is a stronghold in creative software, but its shares have been pressured by recent executive departures and intensifying competition from artificial intelligence.

Which stock is better for long-term investment?

Both are good compounders. Microsoft makes for more natural long-term holding, for sleep-well stability and rising dividend. Adobe is an interesting case for value if the moat holds up to AI, but it's not a case of it dying. It is not the quality of the business, it's what you pay for it.

Does Adobe risk AI disruption?

Yes, this is the main issue and why it's affordable. The competition from generative tools from OpenAI, Google and Midjourney could threaten Adobe's moat in the long term. The rebuttal is that Adobe is also making an aggressive play with AI (Firefly has 70M+ users) and the market is already building in a strong degree of pessimism, at about 1.7% implied growth. There is a risk involved and there is a discount involved.

How does Copilot compare to Firefly?

Copilot is a productivity assistant integrated across Office 365, Windows and Teams that is primarily designed for enterprises (nearly 70% of Fortune 500 companies use it). Firefly is a suite of creative generative AI tools integrated into Adobe design tools, with 70M+ users and direct revenues of ~$400M. Copilot is an extension of Microsoft's existing moat. Firefly continues and builds upon Adobe's.

References

- Adobe Inc. (2025). Adobe fiscal year 2025 annual report. Adobe Investor Relations. View Source

- Microsoft Corporation. (2025). Microsoft fiscal year 2025 annual report. Microsoft Investor Relations. View Source

- Macrotrends. (2026). Microsoft (MSFT) financial statements 2010–2026. View Source

- Macrotrends. (2026). Adobe (ADBE) financial statements 2010–2026. View Source