NVIDIA is priced for perfection. At a market cap of roughly $5 trillion and a share price near $208, the Financial Beings residual income model implies a long-term growth requirement of about 8% — a level that very few companies have sustained at this scale. At 7.5% growth, intrinsic value falls to $156 per share. At 8.5%, it rises to $255. That is the entire trade. The question for 2026 is not whether NVIDIA is a great business — it is whether a company already approaching $5 trillion can compound above 8% for the next decade. Only three cents of every dollar in today’s price is backed by current fundamentals. The remaining ninety-seven cents is expectation.

Is the valuation justified? Expectations can answer this.

Is NVIDIA Stock a Good Buy Right Now in April 2026?

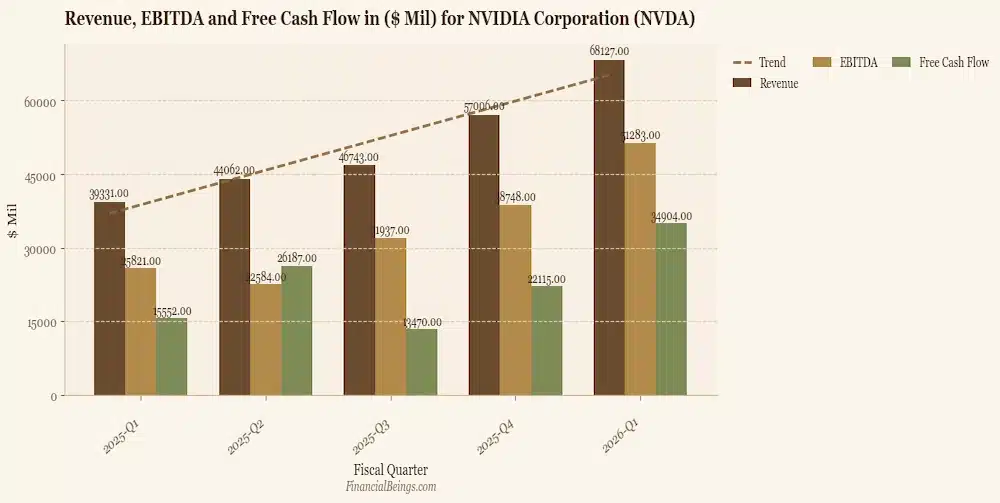

By the middle of April 2026, NVIDIA is strategically positioned into the global artificial intelligence (AI) ecosystem, but a major provider of AI infrastructure. Its development is powered by the high demand for GPUs in data centres, where the process of training and deploying AI models is rapidly growing. Its quarterly revenues stood at about $68.1 billion with a year-on-year growth of 73% percent and gross margins of over 70%, which indicates strong pricing power and a high level of efficiency in its operations. Its technological leadership is further supported by high-tech architectures like Blackwell and future architectures like Rubin.

Moreover, NVIDIA will resume its business, which will boost the company in terms of revenue in 2026. Although the company is still seen as having a good financial performance and an international expansion rate, its valuation includes a high potential for growth in the long-term, especially the adoption of AI. Investors seeking a broader perspective on how NVIDIA compares with other leading technology companies can also review the Meta vs NVDA Stock Analysis for a deeper valuation and growth comparison. Altogether, the situation at NVIDIA in April 2026 can be characterised as an interplay between good operational results and a progressive growth strategy with the focus on the development of AI.

Financial Beings Valuation Lens

NVIDIA Stock Price Forecast and Targets 2026–2030

Using only the Financial Beings valuation model, here are the price levels that correspond to different embedded growth rates (g) at the 2026 horizon:

- At g = 7.5%, value per share is $156.13.

- At g = 8%, value per share is $193.54.

- At g = 8.5%, value per share is $255.90.

- At g = 9%, value per share is $380.61.

2026 Outlook

The stock can move from $199 to around $256 over the next twelve months if the AI cycle pushes the market’s long-term growth expectation higher by roughly 50 basis points. However, that re-rating must be supported by earnings delivery, not just sentiment.

The reverse dynamic is equally important. If earnings disappoint and AI enthusiasm fades, the market compresses its embedded growth assumption by 50 basis points, and value per share falls toward $156 — implying roughly a 22% downside at a 10% hurdle rate.

What happens to NVDA in 2026 is primarily a function of whether AI sentiment and earnings delivery push the embedded growth rate higher or lower, rather than the underlying hardware cycle itself.

2030 Outlook

To illustrate how powerful this sensitivity becomes over longer horizons, extending the same framework to 2030 simplifies the outcome into three scenarios:

If the market sustains NVDA at embedded growth rates between 8% and 8.5%, value per share ranges from approximately $193 to $256 — effectively fair value to moderate upside from current levels.

If the market re-rates NVDA toward 9% embedded growth, value per share increases to approximately $380. This reflects the convex acceleration in the residual earnings framework as growth approaches the hurdle rate.

In summary, the range of outcomes for NVDA in 2030 is not constrained by its engineering capabilities or customer demand. It is constrained by what level of perpetual growth the market is willing to underwrite.

Sustaining an embedded growth rate above 9% is historically rare, although not without precedent — Microsoft achieved this during its cloud transition. In contrast, sustaining growth below 8% is far more common.

Financial Beings Interactive Chart

| Growth (%) | Model Value ($B) | Model Price/Share | Model Value % |

|---|

Model Value % > 100% = The model value exceeds the current market cap under the stated assumptions. Model Value % < 100% = The current market cap is above the model value under the stated assumptions. Model Value % = 100% = The model value matches the current market cap at the assumed growth rate.

At 2% growth, NVDA’s model value reaches a Model Value % of 26.7% relative to current market cap. Even at 5% growth, the model reaches only a Model Value % of 40.8%, and it does not exceed current market cap until the long-term growth assumption moves just above 8%.

The breakeven growth rate is approximately 8.0%. That is a demanding long-term growth rate expectation for a company already valued at nearly $4.85T, which suggests the market is still pricing in very strong long-run compounding from Nvidia’s AI and accelerated computing franchise.

Note: Under the 10% hurdle rate scenario set, NVDA reaches 128.3% Model Value at 8.5% growth and 190.8% at 9% growth. The steep value ramp at the high end of the range reflects Nvidia’s exceptionally strong ~206% RNOA basis, but the current market cap still implies sustained growth well above a typical mature-company growth assumption.

Investor letter

If you have read this far, you already think differently about investing.

Get valuation research like this delivered weekly. Hard numbers, clear language, no hype, and no sponsored stock picks.

Vera Rubin is a generational leap

Seven breakthrough chips, five racks, one giant supercomputer – to power through every stage of AI. The agentic AI inflexion point has come with Vera Rubin launching the biggest infrastructure construction endeavour in history.

NVIDIA Stock Forecast 2030: AI Growth & Long-Term Outlook

A deep dive into NVIDIA’s long-term price prediction, AI dominance, revenue expansion, and future growth scenarios up to 2030. Explore bullish and bearish outlooks.

Read Full Forecast →NVIDIA Business Model and Unmatched AI Dominance

The business model of NVIDIA is founded on the powerful and integrated ecosystem that enables the development of artificial intelligence (AI) on a global level. Instead of being a semiconductor company, NVIDIA has become a complete AI infrastructure company. Such a strategic change has helped the company to stay in the lead of the market and enjoy the fast growth of AI in the industries. It is leading its pack in terms of technological innovation, as well as control of major aspects of the AI value chain.

Key Elements of NVIDIA’s AI Dominance

- CUDA Software Moat

The NVIDIA CUDA technology is a proprietary system that enables developers to create AI models that are optimised to run on its GPUs. CUDA has, over time, become an industry standard, which has led to high switching costs and customer loyalty.

- Full-Stack Advantage

The company provides a single ecosystem that comprises GPUs, software systems and networking systems. This full-stack solution allows NVIDIA to provide end-to-end AI solutions and enhances its dominance in the infrastructure market.

- Market Share Leadership

The market in AI chips is controlled by NVIDIA, which holds an estimated share of 80-90% of the market. Such leadership enables the company to establish industry standards and to have a direct advantage in the global AI adoption.

- Diversification Beyond Gaming

NVIDIA no longer deals with gaming and has turned to data centres, which is 90% of revenue, and are now the largest source of its income. This is an indication of its transformation into an infrastructure provider of AI computing.

In general, the power of the NVIDIA ecosystem, software base and market penetration remains to underpin the leadership in the global AI market.

NVIDIA Earnings and Revenue Growth (2026)

NVIDIA (NVDA) announced impressive financial results for fiscal 2026, with annual revenues increasing by 65% growth rates on a year-over-year basis, to $215.9 billion. The revenue of the data centres was the key driver, with $193.7 billion, which is an increase of 68 per cent compared to the year before, driven by the need to acquire the Blackwell AI chips. In 2026, Q4 saw a revenue of $68.1 billion and GAAP earnings of $1.76 per share.

- NVIDIA (NASDAQ: NVDA) today announced a record revenue of the fourth quarter ended January 25, 2026, of $68.1 billion, an increase of 20 per cent compared to the prior quarter, and 73 per cent compared to a year earlier. For fiscal 2026, revenue was $215.9 billion, up 65% from a year ago.

- NVIDIA expects further strong growth in Q1 2027 (ending April 2026) and revenue of about $78 billion due to the large usage of AI agents in the enterprise.

- The company is experiencing high demand for its Blackwell and future Rubin chip platforms, with a $1 trillion revenue stream expected to come in 2026 and 2027.

- NVIDIA is highly profitable and has financial performance with gross margins of ~75% in Q4 FY2026 (GAAP 75.0%, non-GAAP 75.2%) and full-year margins of over 71%, and Q1 FY2027 is projected to be similar. The growth in earnings is also high, with Q4 EPS of $1.76 (an increase of 98% YoY) and full-year EPS of $4.90 (an increase of 66.67% YoY), and estimating a further increase at approximately 65.6%.

Moreover, NVIDIA has a high cash generation & operational efficiency with Q4 free cash flow of $34.9B (51.2% margin) and a total of approximately $96.68B annually (58.87% margin), as well as the annual growth of cash generation and operational efficiency of 58.87%.

Is NVIDIA Overvalued or Fairly Valued in 2026?

One of the most crucial factors to analyse NVIDIA in 2026 is valuation. The company is trading at a higher price-earnings ratio than the traditional semiconductor companies, and this begs the question as to whether the company is overpriced.

However, what is more significant is to know what the present price is telling us about the future. With a share price of around $208 and a market value of around $5 trillion, only three cents out of every dollar is backed by current fundamentals, with the rest considered to be expectations of future growth.

In deconstructing the valuation, the market seems to anticipate a long-term compound growth rate of about 8.67% perpetuity. This is a challenging product to expect because few firms have been able to maintain such growth rates over time, like Microsoft.

This underlines the main contradiction in the valuation of NVIDIA: the company is obviously in a good position, yet the price is already based on a highly optimistic future.

NVIDIA (NVDA) Stock Analysis Post Q3 FY25 Earnings

A deep dive into NVIDIA’s AI dominance, revenue growth, and future outlook. Discover whether NVDA is still the best AI stock to buy in 2026.

Read Full Analysis →NVIDIA vs AMD: Comparative Analysis

By April 2026, the AI market will have NVIDIA (NVDA) with a better increase in revenues (more than $68B in Q4 FY2026 revenue) and margins, and AMD with better growth prospects (increasing market share and a more diversified portfolio). NVDA is considered to be the less risky, dominant leader, whereas AMD is the high-upside option.

| Factor | NVIDIA (NVDA) | AMD (Advanced Micro Devices) |

| AI Market Share | ~80–90% of the AI accelerator market | ~7–20% share, growing gradually |

| AI Data Centre Revenue Share | ~86% dominance in AI data centre GPUs | ~7% share, expanding with new deals |

| Ecosystem Strength | Strong CUDA software ecosystem (high switching cost) | ROCm ecosystem is developing but less mature |

| Revenue Growth | ~62–65% growth rates in recent periods | ~30–35% growth, slower than NVIDIA |

| Profitability (Margins) | Higher margins (~70%+ gross margins) | Lower margins, more price competition |

| AI Strategy Focus | Training + inference + full-stack infrastructure | Focus on inference + cost efficiency |

| Key Strength | Market leader, full-stack AI platform | Challenger with strong partnerships (e.g., Meta, OpenAI) |

| Competitive Position | Industry leader sets standards | Fast-growing competitor, gaining share slowly |

NVIDIA vs AMD AI Dominance 2025: Who Will Lead the AI Revolution?

A detailed comparison of NVIDIA and AMD in the AI chip race, covering market share, GPU performance, software ecosystem, and future leadership in AI computing.

Read Full Comparison →Major Risks of Investing in Nvidia Stock

The main threats to Nvidia (NVDA) stock in the year 2026 will be excessive dependence on AI capital expenditure, high valuation risk, competition from custom chips and geopolitical exportation. As a percentage of revenue, 91% of it now comes via data centre customers, and any decline in AI investment could have devastating consequences on growth. The low concentration levels in the market imply that the stock is likely to experience steep corrections.

The main risks of investing in Nvidia stock:

- Reliance on AI Spending: Approximately 91% of revenue is from data centre customers; a decline in hyperscaler spend could have a drastic effect on demand and growth.

- Intense Competition & Custom Chips: This can be mitigated by increasing competition from AMD, Intel, and custom AI chips (ASICs) by Amazon and Microsoft, making it less dependent on NVIDIA GPUs.

- Geopolitical & Regulatory Risk: U.S. export policies restricting the export of highly sophisticated AI chips to China are generating uncertain revenues and inventory.

- Valuation Vulnerability: NVIDIA is a high-growth, high-beta stock, which is vulnerable to macroeconomic conditions and might be subject to sharp corrections.

- Supply Chain Concentration: The overdependence on TSMC in production poses a potential risk in production.

- Market Concentration Risk: The business relies on a few big clients, which makes it more exposed in case their investment rate is decreased.

Conclusion

The NVIDIA in 2026 is a powerful long-term growth narrative that is driven by its dominance in artificial intelligence and data centre infrastructure. Is Nvidia (NVDA) a Good Stock to buy in 2026 best fits long-term growth investors who are comfortable with volatility and realise that much of its value is pegged on future expectations. Its lead in AI, good financial results and constant innovations come as evidence of the long-term potential of the company. Nonetheless, it might not be appropriate for short-term or risk-averse investors, because the stock is susceptible to market factors, valuation, and fluctuations in AI expenditure.

Strategically, strategies such as dollar-cost averaging (DCA) might be used to control the timing of entry and minimise the risk, though moderate portfolio allocation should be maintained because of concentration risks. In sum, NVIDIA embodies both solid business underpinnings and elevated market expectations, implying that its performance will rely on its capacity of maintaining growth in the dynamic AI environment.