Adobe intrinsic value vs expected return: ADBE trades at $236 with $264–$359 intrinsic value. See what the analysis reveals about owning ADBE now.

We use the residual income model to calculate intrinsic value of Adobe and compare it with the required return. The following are the numbers on owning ADBE at the current prices.

Adobe is underpriced now in comparison to its current market price, which is measured on the basis of a residual income model. It can be found that the intrinsic value per share of Adobe is between $264 and $359, whereas the market reference is around $236, which means there is 11% to 51% percent upside on a realistic growth case.

The market is valuing Adobe in a manner that its long-term growth is structurally weak. The growth rate implied in the prevailing price is around the mark of ~2.4%, which is significantly lower than the historical growth trend, as well as the operations performance of Adobe.

Adobe is not a failed growth story. It is a high-quality compounder that is currently valued as a low-growth company, and this has provided a perfect opportunity to value it based on a market-pessimistic rather than a business-pessimistic scenario.

| Growth (%) | Intrinsic Value ($B) | Price per Share ($) | V/P (%) |

| 2.0% | 96.49 | 235.05 | 94.9% |

| 3.0% | 108.61 | 264.58 | 106.8% |

| 4.0% | 124.78 | 303.96 | 122.7% |

| 5.0% | 147.41 | 359.09 | 145.0% |

| 6.0% | 181.35 | 441.78 | 178.4% |

| 7.0% | 237.93 | 579.60 | 234.1% |

| 7.5% | 283.19 | 689.86 | 278.6% |

| 8.0% | 351.08 | 855.25 | 345.4% |

| 8.5% | 464.23 | 1130.89 | 456.7% |

| 9.0% | 690.54 | 1682.18 | 679.3% |

What is Adobe’s intrinsic value in 2026?

Adobe’s intrinsic value in the year 2026, is around $264 to $359/share, a value lower than the current market value of about $236/share, which means that the stock is trading at 11% to 51% discount on the reasonable assumptions of growth.

The long-run growth assumption is essential to Adobe’s and is intrinsic values, the point is that the stock does not need aggressive growth to look appealing. Considering a slow growth rate of 2 per cent, the model would give an intrinsic value of $96.49 billion and $235.05 per share, which is a little lower compared to the present market value. Nonetheless, any increase in growth assumptions is significant to cause a significant change in valuation.

With a growth of 3 percent intrinsic value is increased to $108.61 billion and $264.58 per share and the stock is undervalued. At 4 percent growth, the value is further increased to $124.78 billion and $303.96 per share and at 5 percent growth, the value is further increased to $147.41 billion and $359.09 per share.

More than any point of valuation, this development is crucial. It demonstrates that the valuation support is developed in a short period, and slight variations in growth expectations are observed. Adobe is almost fairly worth 2%, is undervalued 3% and is grossly undervalued 5%. This would imply practically that it does not require the company to do something out of the ordinary to warrant upside, just the maintenance of modest, sustainable growth.

Value-to-price (V/P) relationship also supports the same conclusion. With a growth of 2 percent, V/P is under 100 percent showing minimal overvaluation. It however tops 100% at 3%, 122.74% at 4% and 145.00% at 5% and depicting an upward trend of to levels of undervaluation as growth assumptions normalize.

The current market-implied growth rate of the company stands at almost 2.4% is thus structurally inconsistent with the prior operating profile and long-term forces of demand of the company, which is why the stock is being priced with an excess of caution instead of with the level of business strength that the company had in the past.

Our valuation methodology: why residual income, not DCF

The residual income method is better than the discounted cash flow (DCF) method of valuing Adobe as it bases its calculation on the available financial performance and does not establish long-term forecasts. Traditional models of DCF demand the projection of free cash flows deep in the future and the estimation of the terminal value that frequently ends up being the biggest and the most uncertain part of the valuation. Minor alterations in assumptions including growth rates or discount rates can cause a big difference in the final result.

On the contrary, the amount of residual income starts with book value that has been previously stated in the balance sheet and goes on to take the value of creation above cost of capital. This forms a clearer and less volatile system of valuation. Rather than seeking to know what cash flows may be in the far future, the model seeks to determine how effectively the company is making returns on its operating assets today.

This is especially in the case of Adobe. Being a light capital-intensive software company, it is valued based on high margins, recurrence revenues, and high operating efficiencies as opposed to extreme reinvestment on physical assets. Return on Net Operating Assets (RNOA) makes it possible to directly include this efficiency in the model.

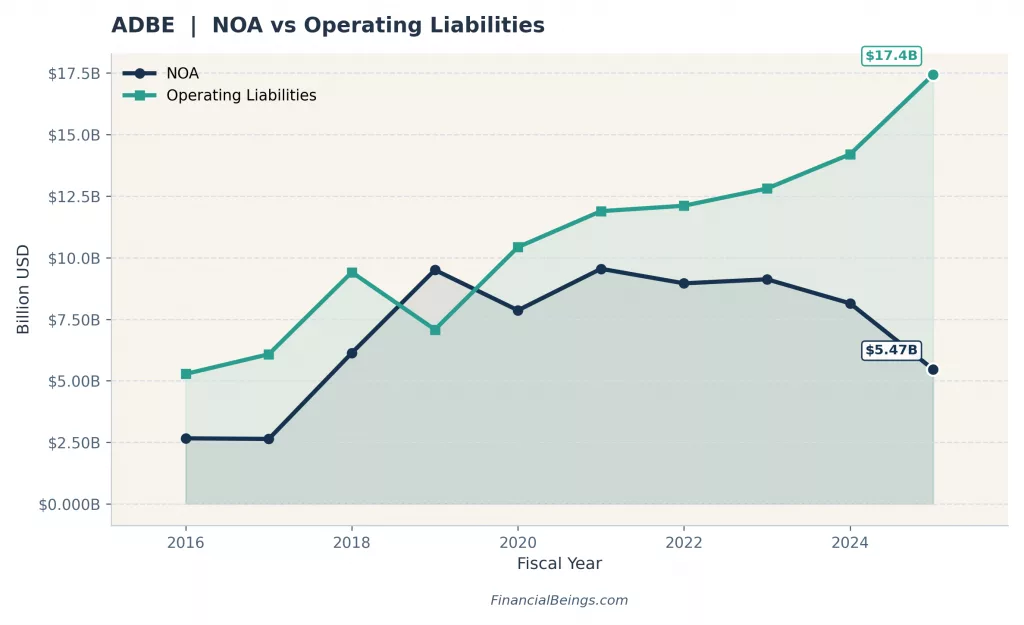

Figure 3: Net Operating Assets vs Operating Liabilities (2016–2025)

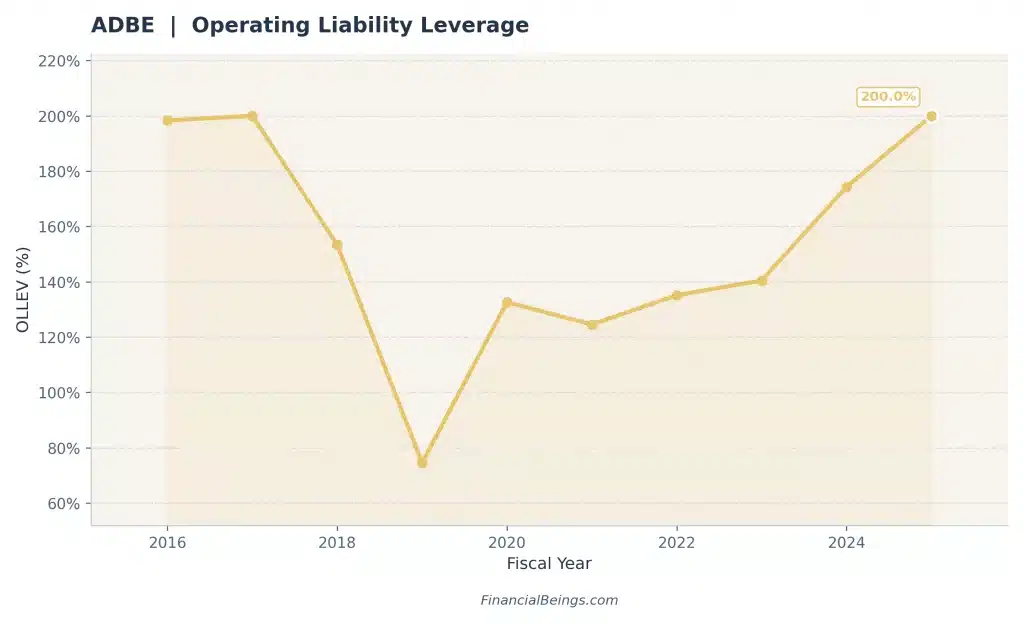

Figure 4: Operating Liability Leverage Trend (2016–2025)

Altogether, the residual income model is rather congruent with the economic reality of Adobe. It puts emphasis on value creation in the form of profitability and capital efficiency which is more reliable in this situation compared to DCF as a means of determining intrinsic value.

Why residual income outperforms DCF for software companies

Residual income model is better than the traditional (DCF) approaches to software companies due to its lower and more valid assumptions. The model bases valuation on book value, which has been recorded on the balance sheet, instead of projecting free cash flows further into the future, and this gives it a logical and starting point. This goes a long way to increase the insensitivity to the assumptions made about terminal value, the easiest part of DCF models that is uncertain.

Moreover, the model also uses Return on Net Operating Assets (RNOA) as its fundamental profitability measure. RNOA is a better measure of economic performance in capital-light software companies such as Adobe where efficiency and growth of value are determined by expanding returns on a lighter asset base. The operating leverage of Adobe brings out the high returns per relatively tiny operating base, which proves the power of a high operating leverage, so residual income is the valuation lens that is analytically suitable.

Key inputs our model uses – and what they signal about Adobe

The model relies on three fundamental inputs and these are; book value, net operating assets (NOA) and cost of capital. The book value and the NOA also have their foundation on the balance sheet of Adobe, meaning that the valuation is not of speculative forecasts, but of what is actually observed in the financial records. This enhances the reliability and minimizes model risk.

A company that is persistently generating returns exceeding its cost of capital cannot be valued at a very high discount rate. The continuation of economic value creation since 2021 in the case of Adobe justifies an anchoring of the cost of capital towards the low end of what otherwise would have been determined to be attributed to high-multiple software companies.

We set the hurdle rate to 10 percent (a fairly high rate) due to pessimism of investors over AI integration in its current products and profits future profits from the products. Since Adobe has been making profits consistently over its hurdle rate cannot be valued as shown by the current market price as though its operating engine is structurally impaired.

Adobe intrinsic value analysis: per share, price target, and Peer Comparison (Interactive Chart)

The intrinsic value of Adobe, when evaluated using a residual income model, will demonstrate a resounding lack of alignment between market prices and business performance. The underlying-valuation presupposes 3%-5% percent growth rate in the long term, but it is rather modest when compared to the previous trend of the company and its present operating sustainability. Based on this, intrinsic value per share is projected at between $264 and $359 as compared to a current market value of around $236 as an upside potential between 11% and 51%.

| Growth (%) | Intr. Value ($B) | Price / Share | V/P % |

|---|

V/P > 100% = The stock is undervalued. Intrinsic value exceeds the market price; you are getting more than you are paying for. V/P < 100% = The stock is overvalued. The market price exceeds intrinsic value; the price embeds growth expectations the model hasn’t yet confirmed. V/P = 100% = The stock is fairly valued. Price equals model value at the assumed growth rate.

At 2% growth, ADBE’s intrinsic value sits just below its current market price at 94.9% V/P. The model turns undervalued almost immediately above that threshold — reaching 145.0% V/P at 5% and an extraordinary 679.3% V/P at 9% growth.

The breakeven growth rate is approximately 2.0-2.5%, well below Adobe’s historical operating trajectory — which signals the market may be under-pricing Adobe’s durable competitive advantages in creative software and digital experience platforms.

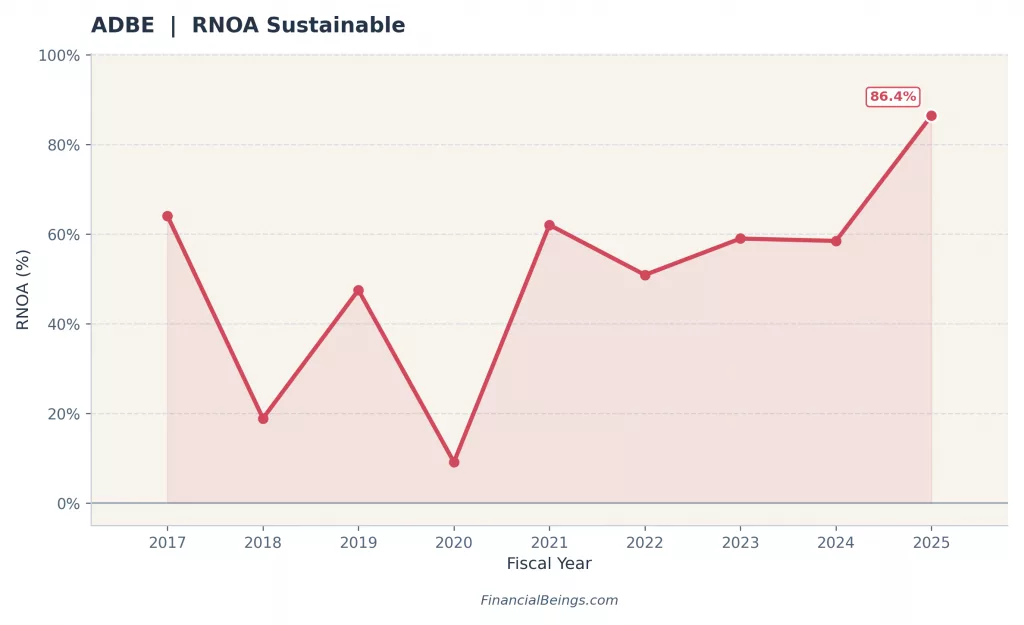

Note: Adobe’s low breakeven growth rate (~2.4%) relative to its historical performance suggests an asymmetric risk/reward profile. The magnitude of V/P expansion at even modest growth rates reflects ADBE’s capital-light business model and high RNOA of ~86.4% (FY2025), which compounds value rapidly through reinvestment at returns far exceeding the cost of capital.

Figure 1. Adobe intrinsic value sensitivity versus long-term growth assumptions (2026–2030 forecast window).

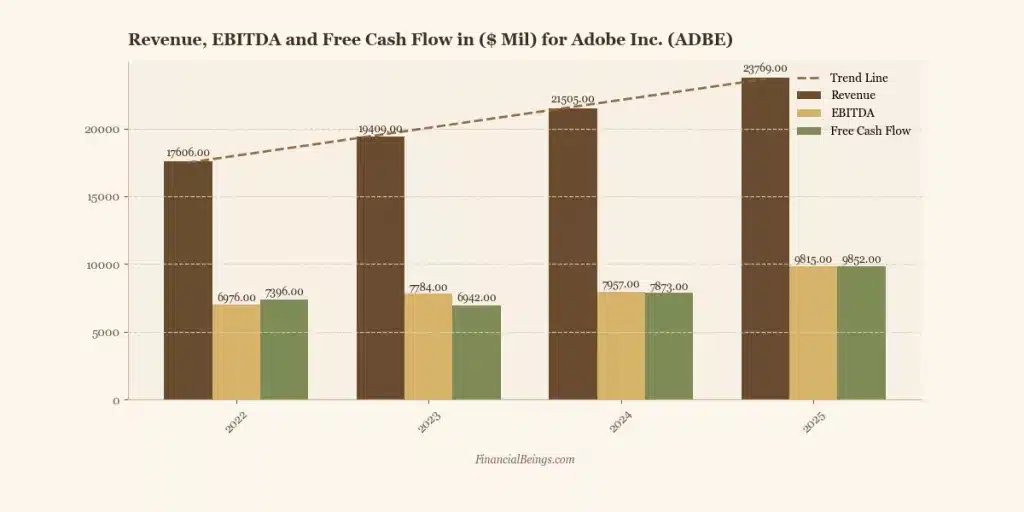

Figure 2: Revenue, EBITDA, and Free Cash Flow Growth (2022–2025)

Adobe has been able to perform well financially behind this valuation. The company has managed to maintain a very high margin and gross margins have been rising exceptionally, as the gross margins have risen in 2022 and then in 2025 to 87.70% and 89.27% respectively, whereas the operating margins have been improving, which stood at 34.64% and 36.63% in 2022 and 2025 respectively. Strong cost control and pricing power could be seen in the net margins of 30.00% in 2025. Simultaneously, revenue grew to $23,769 million as compared to the previous year of $17,606 million and free cash flow rose by $9,852 million meaning that the company produced a lot of cash.

All these trends ensure that the business model of Adobe remains efficient and sustains the intrinsic value growth (3%-5%) without the need to make aggressive assumptions.

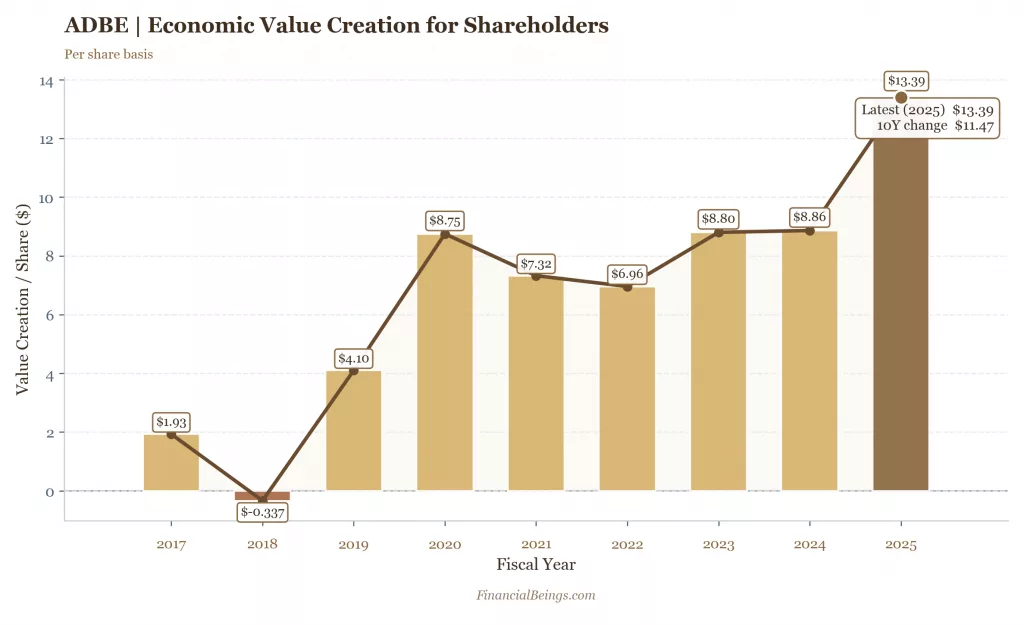

According to this range of valuation, a sensible price target is between $300 and $360 per share which is the average of the base-case scenario. This target is a normalization of market expectations and not fundamentals. Notably, Adobe does not require a remarkable growth to achieve this level; it just requires to maintain its present profile of operations. The capacity of the company to create economic value is also evident in the fact that value creation per share increased by 2025 to $13.39, indicating the high trend of shareholder returns.

The valuation argument is further enhanced by a comparative point of view. Rather than making the conventional multiples, a more valuable comparison is made using market-implied growth rates. The current Adobe implies a current growth rate of about 2.4%, as opposed to comparable companies like Microsoft and Salesforce whose growth implication is above 6.5%. This disparity implies that Adobe is being under-valued even though it is showing similar levels of profitability and efficiency.

Adobe’s Return on Net Operating Assets (RNOA) has been at about 86.4%, meaning that the company has been very capital efficient. This is a very high payoff, which can result in sustained value creation even when there is a moderate growth assumption. Consequently, Adobe seems to be underestimated in terms of growth-adjusted value basis, which supports the perspective that the existing valuation is due to the prevailing market conservatism, as opposed to any underlying vulnerability.

Figure 5: Economic Value Creation per Share (2017–2025)

Adobe intrinsic value per share: base case

The price base-case estimation will be under the 3%-5% long-term growth range that is still very conservative considering the operating trends and market positioning of Adobe. Intrinsic value per share is estimated between $264 and $359, which reflects between a range of 11% to 51% upside potential.

Adobe is a well run business that justifies this valuation. The gross margins have continued to improve as it stood at 87.70% in 2022 to 89.27% in 2025 and operating margins have gone up to 36.63% to 34.64% respectively. The net margins also hit 30.00 percent in 2025, which indicated steady profitability. Simultaneously, the revenues increased by nearly 5.5 times in 2022 to $23,769 million in 2025, and free cash flow became $9,852 million, which testifies to the power of cash generation at Adobe.

These ratios suggest that the intrinsic values of Adobe are not subjected to aggressive presumptions. It is rather pegged on long-term profitability, efficiency in its operations and average growth prospects that are consistent with previous performances.

Price target based on Adobe’s intrinsic value

The price target will be calculated based on the intrinsic range of the value of $264-$359 per share, and the base-case target will be in the range of $300-$360. This valuation is market expectations being normalized as opposed to a change in fundamentals, i.e. it does not mean that Adobe would need extraordinary growth in order to attain this valuation.

The reasoning behind this target is that Adobe is improving its economic value creation and operation efficiency. The growth of economic value creation per share has been positive between 2022 and 2025 with the figure of $6.96 and $13.39 respectively, which is a good trend in terms of shareholder value creation. Also, Adobe has a high operating leverage as is indicated in the capital structure where operating liabilities of the company in 2025 amounted to about 17.4 billion as compared to net operating assets of about $5.47 billion. This explains that Adobe does not require high asset base and they use their liabilities efficiently.

Adobe vs big tech intrinsic value: how does ADBE compare?

Another superior means of measuring Adobe valuation is by applying market-implied growth rates, as opposed to traditional valuation multiples. The respective current market price shows that the market is expecting that Adobe will grow in the long-term by about 2.4 per cent on average, much lower than its competitors, including Microsoft and Salesforce, whose market implied growth rates are over 6.5%.

This gap implies that Adobe is being under-priced compared to other similar software firms, even though they are showing the same or better operating efficiency. As an example, the Return on Net Operating Assets (RNOA) of Adobe has already reached about 86.4% in 2025, which means high levels of capital efficiency. This degree of profitability is conducive to generation of values in the short term even in moderate growth assumptions.

This connotation is obvious, as Adobe seems to be cheap on growth-adjusted terms, supporting the idea that the market is discounting risk, as opposed to core. This reinforces the argument of convergence of market price to intrinsic valuation once the expectation levels are normalized.

| Operating support indicator | 2022 | 2023 | 2024 | 2025 |

| Gross margin (%) | 87.70 | 87.87 | 89.04 | 89.27 |

| Operating margin (%) | 34.64 | 34.26 | 36.00 | 36.63 |

| Net margin (%) | 27.01 | 27.97 | 25.85 | 30.00 |

| Revenue ($ mil) | 17,606 | 19,409 | 21,505 | 23,769 |

| EBITDA ($ mil) | 6,976 | 7,784 | 7,957 | 9,815 |

| Free cash flow ($ mil) | 7,396 | 6,942 | 7,873 | 9,852 |

Adobe intrinsic value sensitivity table: bear, base, and bull scenarios

One important observation during the sensitivity analysis is that even with very small growth assumptions, valuation support becomes apparent. In comparison to high-multiple AI names, which need a high long-term growth to warrant their price, Adobe achieves a fair upside value in a range of 3%-5%, which incorporates a substantial decrease in the execution risk. It implies that this stock will not rely on the optimistic forecasts, but rather, it will be backed by conservative assumptions, which will make the valuation framework stronger and more dependable.

| Scenario | Growth assumption | Intrinsic value ($B) | Price/share | V/P |

| Bear | 2.0% | 96.49 | 235.05 | 94.92% |

| Base | 3.0%–5.0% | 108.61–147.41 | 264.58–359.09 | 106.84%–145.00% |

| Bull | 6.0%–7.0% | 181.35–237.93 | 441.78–579.60 | 178.40%–234.05% |

Bear case – intrinsic value and key assumptions

The bear case is that the long-term growth rate will be about 2% and this is a situation in which Adobe will have a slower growth rate as a result of competitive forces, or price restraints or a decline in margins. Based on this assumption, intrinsic value per share will be approximated to be about $235, which is a bit lower than the current market value ($241).

This situation suggests that the market already assumes a close to a worst-case scenario. The negative is not expected to be very high even in case the growth has slowed significantly, as the high margins and recurring revenue base of Adobe creates a valuation floor. Intrinsic value at 2% growth rate that is slightly lower than the current market cap communicates to investors that they have a good margin of safety because the stock is already trading at even lower growth rates than the longterm nominal GDP of the US.

The most important conclusion from the bear case is that massive downside would imply structural degradation of fundamentals, which cannot be seen in financial performance in Adobe.

Base case – intrinsic value and key assumptions

The base case presumes the growth of between 3-5 percent per long-term, which is consistent with the history of Adobe and its business demand. In this case, the intrinsic value per share is between $264 and $359 that is obviously higher than the existing market price.

Adobe has the capability to earn returns that are above its cost of capital; hence this valuation. The company still shows good operating performance whereby revenue has gone up to $23,769 million, free cash flow has been up to $9,852 million and the margins have always been high. These aspects show that the operating engine of Adobe has not faltered.

The base case points out that even conservative assumptions have positive upside. The stock does not necessarily require any extraordinary growth to provide returns; it just should be stable, and remain efficient. This reduces the execution risk by a large margin and encourages valuation growth.

Bull case – intrinsic value and key assumptions

The bull scenario presupposes the growth rate between 6 and 7 percent, which represents the increased demand, especially due to the integration of AI product and the development of digital experiences platforms. In this case, intrinsic value per share is hugely high at an average of $441-$579.

This advantage is fueled by the capacity of Adobe to maintain high returns on capital in as much as it increases its business. As RNOA stands at about 86.4%, the company is highly efficient in utilizing the operating base to make a profit. When this performance is sustained together with the increased growth rate then the compounding effect in the valuation is very high.

Also, Adobe has created its shareholder value to a better economic value of $13.39 per share, which confirms that it is capable of creating shareholders value in the long run. The bull case thus is not only an increase in the growth, but also sustainability of good profitability and operating leverage, in short, market dominance.

At what price does Adobe become a clear buy?

Adobe would be an easy buy when price is near enough to the lower end of the intrinsic value band where the margin of safety is at its best. According to the sensitivity analysis, this level is approximately $260 per share and the extent of the gap in valuation starts to grow significantly in most instances. Investors who want to take position in ADBE can consider it as it is trading near the valuation floor due to market over-pessimism. The stock at around $235 is at the bear-case valuation which is at a point where the downside risk is very low as compared to intrinsic value.

At such levels, the gap in valuation will be virtually zero with conservative assumptions, i.e. the investors are already paying a price that already reflects low growth expectations. This provides a good risk-reward profile of having a minimal downside and the upside is not compromised.

Here, the principle of margin of safety is essential. Lowering entry price lowers dependence on the growth assumptions and chances of positive returns are higher. The set of solid foundations and cautious pricing positions in the case of Adobe offers a clear guideline of the establishment of attractive entry points.

Adobe’s expected return: what investors get at current price

The current stock price is likely to give Adobe’s shareholders a 7.7%-9.6% payoff, if they invest at the present price, assuming a 3%-5% growth rate over the long term and a cost of capital of 10%. This payoff is calculated directly from the residual income model, that is, it is the expected return if investing at the current market price. The risk is low however the return is high making risk-reward ratio robust.

The relevance of this profile of returns is that it is stable. Adobe is able to provide competitive returns under moderate assumptions, unlike high-growth technology stocks, which require rapid growth to be justified by valuation. The expected returns are also positive even in lower growth levels and backed by good margins, recurrent revenues, and good capital usage. At gross margins of nearly 90 per cent and operating margins of over 36 per cent, Adobe is still making steady gains and this is what is directly transferred into projected profitability.

The market expectations are however compressing the anticipated profile of returns. The market is implying that Adobe is growing at a rate of about ~2.4%, which is lower than its historical growth and ability to achieve this growth. This squeeze is not motivated by the weakening of fundamentals but fake danger, especially in the area of AI disruption and competitive positioning.

Figure 6: Sustainable RNOA Trend (2017–2025)

This creates a key asymmetry. In case Adobe does not change the level of current operating performance, anticipated returns will be appealing. In case the growth expectations are normalized to even small levels, the returns would be better. The valuation hence does not involve positive surprise, but only the lack of a negative surprise.

Investors in real world situations are being rewarded to accept perceived risk which is not entirely backed by financial performance. It is this lack of congruence between expectation and reality that makes the opportunity.

The verdict: should investors buy it?

Adobe can be considered a BUY at current levels not because the company is being framed as a high-growth AI stock, but because it is an established compounder that is being underpriced by the market.

This mispricing is mainly caused by the expectations of the market growth. As implied growth, ~2.4% Adobe is trading as though structural slackness in its long-term growth. This supposition is contrary to its financial results, which demonstrate the further growth of revenues, high level of free cash flows, and stable profitability. The margins are also at their highest level in software industry and economic value creation will continue to rise, which means that core business will not be weakened.

Besides, intrinsic value offers coverage when there are conservative assumptions. A valuation is not only above the present price but a margin of safety is also provided even at low growth rates. This minimizes negative risk and maintains the possibility of upside.

AI disruption and competitive force is the main threat. Nevertheless, this risk can be already considered in the existing valuation. Consequently, the payoff profile is skewed: there will be a small downside in the event that pessimism is sustained, but a positive payoff in the event that the expectations are normalized.

To sum up, Adobe can be viewed as a quality business that is underestimated by the market sentiment in the short term, which is why it is an appealing investment in its current condition.

Portfolio recommendations: should you own Adobe in 2026?

Growth portfolio

In the case of growth-oriented portfolios, the Adobe Company can be a very promising company given that it has an asymmetric upside potential in the case of a higher growth scenario. When the long-term growth rate rises up to the 6% to 7% range, intrinsic value is increased by large margins, resulting in a huge upside for growth investors. This translates into a low risk- high reward scenario.

But to bring this scenario to reality, Adobe will need to continue increasing revenues by creating new products, especially in AI-based creative solutions and online experience platforms. Although the company already shows good revenue growth (up to $23,769 million), the case of growth portfolio presupposes further growth based on the monetization of new capabilities.

The most important aspect of Adobe is that it does not need extreme assumptions in order to provide upside to growth investors. Even a moderate increase in the expectations of growth can produce significant returns. Consequently, Adobe presents a strong quality, scalability, and valuation growth opportunity profile, and thus, it is fitting to portfolios that require long-term returns on capital and are patient.

Conservative portfolio

In the case of conservative investors who are interested in capital preservation, Adobe is appealing, but this is not because of the growth optionality, but because of its margin of safety. Bear-case valuation indicates an intrinsic value of about $235 per share, which is quite similar to the current values, and thus, the downside risk is not that large, assuming pessimistic scenarios.

Adobe has good operating profile that justifies this defensive positioning. Gross margins of almost 90%, operating margins of more than 35%, and consistent generation of free cash flows of up to $9,852 million give it a stable earnings base. These elements minimize the chance of material degradation of valuation unless it is a basic failure in the business model.

On a conservative side, Adobe has a buy rating of less than about $260 that is more favorable. Bringing it down to the range of approximately $235, the stock has a high margin of safety as it goes in line with the downside assumptions.

Thus, Adobe can be a defensive technology holding, where stability and capital efficiency offer a layer of protection against downside and yet still has moderate potential upside.

Balanced portfolio

In the case of balanced portfolios, Adobe is a perfect mix of stability and upside and, hence, a core allocation. The base-case scenario which presupposes 3%-5% growth will provide the anticipated returns in the interval of 7.7%-9.6%, which is a good compromise between risk and returns.

The positioning of Adobe is especially robust since it is not pegged on just one outcome. Even in the conservative assumptions, the valuation is supported and moderate increase in the growth results in significant upside. This provides a diversified profile of returns that are in tandem with balanced investment strategies.

Moreover, the excellent economic value creation of Adobe at 13.39 per share and high level of capital efficiency as shown by high RNOA of about 86.4% supports this capacity of the company to generate returns in the long run.

A downward movement of the position stock makes the position upgrade more attractive as the price is brought nearer to $260 or less where the margin of safety is better and anticipated returns are higher. In this case, Adobe will provide better downside and upside risk proposition.

Adobe Stock Is Being Priced Like It’s Dying — The Math Says Otherwise

General positioning: Pricing of fear rather than fundamentals is being priced by the market. Adobe is not rated as a high-quality compounder although it is one. Although the risks associated with AI are real, they seem to be exaggerated in the present price and they are providing the opportunity to long-term investors.

All calculations and valuation estimates are FinancialBeings’ own, based on data sourced from SEC filings of ADBE (10K and 10Q), and ADBE investor relations use or reproduction before prior approval is prohibited.

Frequently Asked Questions (FAQs)

What is Adobe’s intrinsic value per share in 2026?

The intrinsic value of Adobe in 2026 will be between $264-$359 per share, assuming a growth rate of 3%-5% in the long term. This would mean an increase of up to 11% to 51% percent compared to the current market level of about $236 meaning that the stock is undervalued bearing in mind the realistic and conservative expectations.

Is Adobe stock overvalued or undervalued right now?

Adobe seems underpriced at present market values since the intrinsic value is greater than the market price based on a medium growth projection. It is being underpriced as the growth prospects over the long term are perceived to be weak, yet the margins, free cash flow, and steady economic value creation are growing, which indicate that the market is overreacting to risks instead of the economic deterioration.

How does Adobe’s intrinsic value compare to big tech?

The market-implied growth rates of Adobe seem to be more appealing with regard to valuation. The market suggests the growth of Adobe is about 2.4% whereas other comparable companies such as Microsoft and Salesforce have a growth of more than 6.5% even though they have the same profitability. This causes Adobe to be relatively lower on a growth adjusted basis which substantiates the concept of valuation mispricing.

What growth rate is priced into Adobe stock?

The current market price of Adobe suggests the possibility of about ~2.4% per annum over the long-term that is very low as compared to its past performance and growth. This is a sign of low expectation and implies that the market is aggressively discounting future prospects, which leaves a gap between current price and intrinsic value in case of more realistic growth assumptions.

At what price should I buy Adobe stock?

The current price at around $236 is a good entry point, however, investors can keep buying the dip because no one knows the bottom but the stock has minimal risk at around $236 per share.

Usama Ali

Usama Ali is the founder of Financial Beings and a self-taught investor who blends classic valuation study with insights from psychology. Inspired by works from Benjamin Graham, Aswath Damodaran, Stephen Penman, Daniel Kahneman, and Morgan Housel, he shares independent, data-driven research to help readers connect money, mind, and happiness.

Disclaimer

The content provided herein is for informational purposes only and should not be construed as financial, investment, or other professional advice. It does not constitute a recommendation or an offer to buy or sell any financial instruments. The company accepts no responsibility for any loss or damage incurred as a result of reliance on the information provided. We strongly encourage consulting with a qualified financial advisor before making any investment decisions.