Note: This data is as of June 29, 2026. Stock prices and financial information change frequently. Please check the official sources for the latest updates.

THE 15-SECOND ANSWER

Two pharma giants. One has an attractive payout and sounds cheap; the other is the owner of the hottest drug company on Earth and sounds pricey. Looking for profits and a reduced cost? Your stock is AbbVie (ABBV). Like the growth machine and willing to deal with the volatility? You own your stock in Eli Lilly (LLY).

The twist most investors overlook, however, is that AbbVie vs. Eli Lilly Stocks are valued for well-above-average growth well into the future in a residual-income valuation, and the “cheap” one is the more aggressive of the two bets. The numbers below demonstrate just why.

AbbVie vs Eli Lilly Stock Overview

The immunology heavyweight at AbbVie (NYSE: ABBV) is responsible for the development of Humira, the best-selling drug in history, and the follow-on drug, Skyrizi, as well as its new product, Rinvoq, which treats psoriasis, rheumatoid arthritis and inflammatory bowel disease.

Humira’s patent cliff would force AbbVie to rethink its growth narrative and shift its business to these two products, along with adding aesthetics and neuroscience to its product portfolio.

Eli Lilly (NYSE: LLY) discovered the weight loss code. It is a manufacturer of GLP-1 medications, which are used to treat obesity and diabetes, including the oral pill Foundayo (orforglipron), which the FDA approved for weight loss on April 1, 2026. Lilly accounts for approximately 60% of the U.S. GLP-1 market. Market cap: About $1.08 trillion, one of the most valuable companies in the world.

AbbVie is a sophisticated heavyweight defending its title after losing Humira. Lilly is becoming a young star on a remarkable run of form. They are both great companies in vastly different places in their journeys. For a broader view of the top healthcare companies, see: Best large healthcare companies.

Stock Performance

The scoreboard over 10 years is far from equal. In the last decade, the stock of Eli Lilly is up about 1,664% from $10,000 to approximately $176,400. AbbVie has made about a 518% return over the same period, which brought $10,000 to about $62,000. The stock outdid the broader market, but not quite Lilly.

Now, zoom forward to 2026, when the competition is much reduced. Neither of the stocks has risen by more than 4-4.5% YTD. The market is settling down after Lilly’s multi-year monster flight, and the field of patient, long-term buyers is just getting started paying attention.

At-a-Glance Snapshot: ABBV vs. LLY

Below is a side-by-side comparison of the key metrics.

| Metric | AbbVie (ABBV) | Eli Lilly (LLY) |

| Share Price (Jun 2026) | $253.35 | $1,208.12 |

| Market Capitalization | ~$448 billion | ~$1.08 trillion |

| Forward P/E | ~15x | ~27x |

| FY2025 Revenue | $61.2B | $65.2B |

| 2025 Revenue Growth (YoY) | +8.6% | +44.7% |

| Q1 2026 Revenue Growth | +12.4% | +56% |

| FY2026 Revenue Guidance | ~$68B | $82–85B |

| Operating Profit Margin (2025) | ~21% | ~37% |

| Sustainable RNOA | 19.6% | 53.5% |

| Residual Operating Income (2025) | $6.3B | $19.9B |

| Market-Implied Perpetual Growth | 8.6% | 8.1% |

| Forward Dividend Yield | ~2.7% | ~0.57% |

| Flagship Drugs | Skyrizi + Rinvoq | Mounjaro + Zepbound + Foundayo |

| Investor Fit | Income · Value | Growth · Long-term |

What Each Stock Is Worth – Our Fair-Value Read

Regular P/E ratios are not without their pitfall. AbbVie’s low multiple is cheap, Lilly’s high multiple is expensive. Neither tells you what growth is already built into the stock, and that is the only question that’s relevant when determining whether or not it’s a good buy right now.

We have a Residual Operating Income (ReOI) model based on the current Return on Net Operating Assets (RNOA) at each company, rather than a guess as to terminal growth rates in a DCF. Each stock has an embedded forecast. Each of these prices assumes the following at a 10% required return hurdle rate:

The Value/Price line equals 100% in the highlighted row; this is the annual growth rate for the price that is assumed today, and it is the same rate of growth that is assumed over the entire life of the process.

AbbVie (ABBV) – Fair Value at a 10% Hurdle Rate

ReOI base: $6.26B, Current price: $253.35. The price suggests that AbbVie is enjoying ~8.6% perpetual growth, which is near the corners of the historically expected range for the stock, and currently coming out of a period of profit decline rather than increase. If you want to know more about AbbVie i will recommend you to check out this details compariosn of ABBV vs JNJ stock.

| Long-term Growth (g) | Fair Value / Share | Value / Price |

| 2% | $42.47 | 16.8% |

| 4% | $57.24 | 22.6% |

| 6% | $86.78 | 34.2% |

| 8% | $175.42 | 69.2% |

| ~8.6% ← today’s price | $253.35 | 100% |

| 9% | $352.69 | 139.2% |

Eli Lilly (LLY) – Fair Value at a 10% Hurdle Rate

ReOI base: $19.85B, Current price: $1,208.12. Lilly requires the same sense of conviction, as its 8.1% implied perpetual growth rate is also about double the long-run economic growth rate. The difference is the quality of the profit-generating business that underlies that demand. Also notice the tremendous asymmetry at 9% growth, Lilly’s fair value is almost double to $2,255.96.

| Long-term Growth (g) | Fair Value / Share | Value / Price |

| 2% | $308.03 | 25.5% |

| 4% | $400.79 | 33.2% |

| 6% | $586.31 | 48.5% |

| 8% | $1,142.86 | 94.6% |

| ~8.1% ← today’s price | $1,208.12 | 100% |

| 9% | $2,255.96 | 186.7% |

The punch line: AbbVie’s price expectations of perpetual growth are coming from a base of declining profits in four of its last nine years and a reasonable RNOA of 19.6%. Lilly requires a profit base that more than doubled in 2025 and a sustainable RNOA of 53.5%. They are both wagers for growth that is greater than the economy. There’s only one with an upwardly pointing high-return engine.

Profitability Quality: RNOA Deep Dive

Return on Net Operating Assets (RNOA) takes out the leverage and financial chatter, showing the efficiency of each company on the capital they manage. It’s an ‘uninflated’ profitability measure from ROE, which can be inflated by debt.

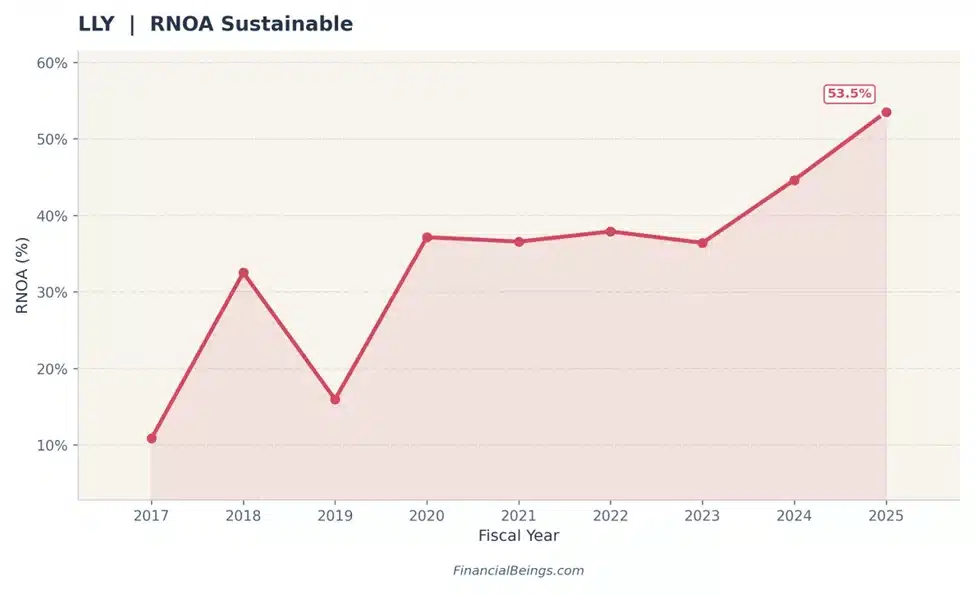

Eli Lilly (LLY) – RNOA Sustainable (2017–2025)

Lilly’s RNOA has improved by almost five times, from 11% in 2017 to 53.5% in 2025, the GLP-1 revenue that has just been exploding while the asset base has been relatively fixed. There was a brief dip to 16% in 2019, followed by a recovery to ~37% through 2020–2023, before the GLP-1 boom powered a steep acceleration to 45% in 2024 and 53.5% in 2025. This level of capital efficiency is very unusual at this scale.

Figure 1: Eli Lilly (LLY) Sustainable RNOA, 2017–2025. RNOA reached 53.5% in FY2025, up from 11% in 2017

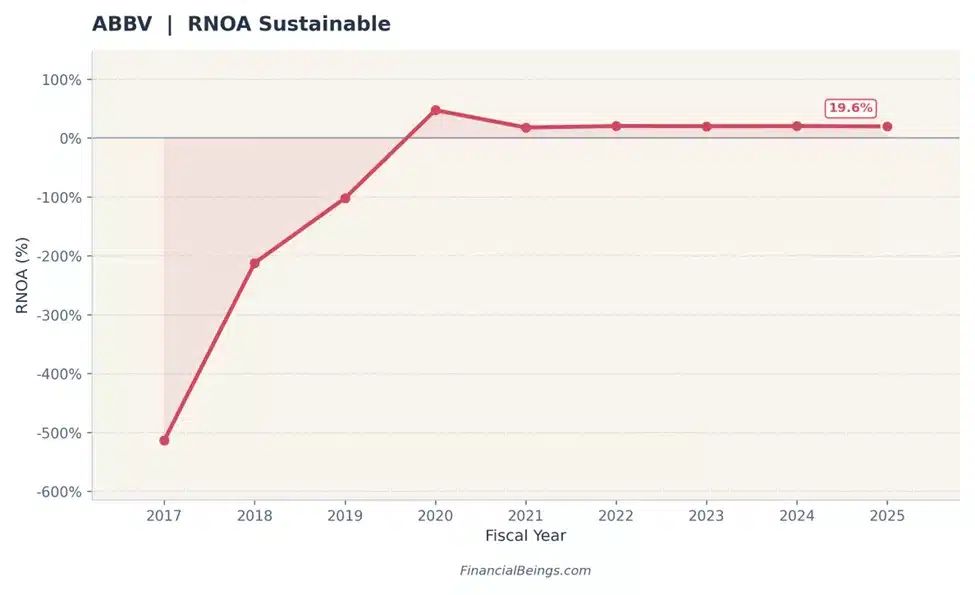

AbbVie’s RNOA track record is quite different. It achieved an extreme negative of more or less -525% in 2017, which was due to AbbVie’s negative net operating assets (mainly negative working capital and deferred revenue since the spin-off). NOA became positive in 2020 upon the Allergan acquisition, and RNOA jumped to ~ +50 % sharply but eventually fell to a stable level of 15-20%.

The latest reading is 19.6% for FY2025 and is virtually unchanged for four years running. The Allergan deal ($63+ billion) is a goodwill allocation that reduces RNOA because the assets are increased, but the operating income is not proportionate.

Figure 2: AbbVie (ABBV) Sustainable RNOA, 2017–2025. RNOA stabilized at 19.6% in FY2025 after the Allergan acquisition normalized the asset base.

In real terms, for every dollar of operating assets employed, Lilly makes 53.5 cents of operating profit. AbbVie generates 19.6 cents. There’s more to the story than size, as Lilly’s is structurally more efficient than AbbVie’s, which is why residual profit is increasing where it is plateauing at AbbVie.

Dividends & Capital Return

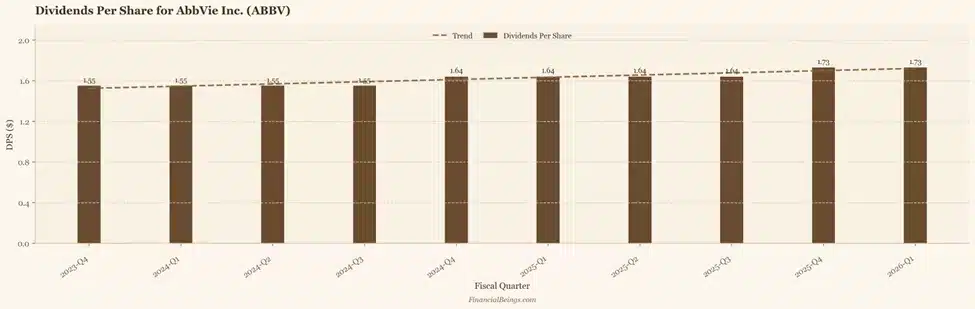

This is AbbVie’s home turf. Inherited from Abbott Laboratories, AbbVie has a pedigree as a Dividend Aristocrat and has increased its quarterly dividend steadily since the 2013 spin-off, from $1.55 per quarter in late 2023 to $1.64 per quarter through 2025 and $1.73 most recently in 2026-Q1. The trend is consistent, predictable and upward.

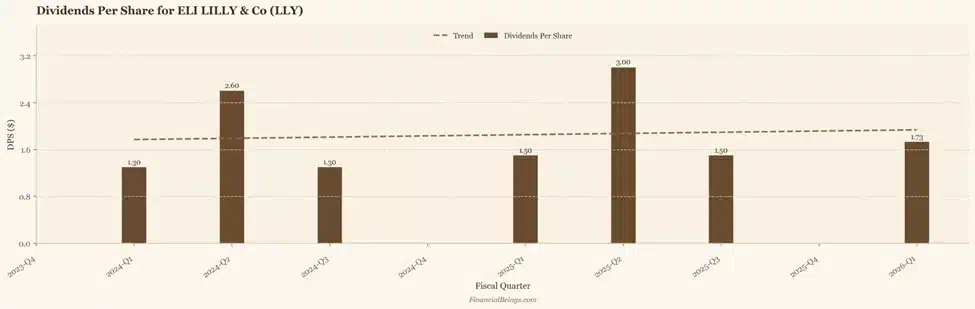

Eli Lilly’s dividend profile is less consistent from quarter to quarter, but it’s expanded as well. LLY paid $1.30/quarter in 2024, raised it to $1.50 throughout 2025, and raised it again to $1.73 in 2026-Q1. Even though LLY now pays the same per-share dividend as AbbVie in the most recent quarter, its much higher share price shrinks the yield to ~0.57%. If you are looking for more high quality dividend stocks, check our list of the Best dividend stocks to buy.

AbbVie (ABBV) – Dividends Per Share

Figure 3: AbbVie (ABBV) Dividends Per Share by Quarter, 2023-Q4 to 2026-Q1. Consistent raises from $1.55 to $1.73/quarter.

Eli Lilly (LLY) — Dividends Per Share

Figure 4: Eli Lilly (LLY) Dividends Per Share by Quarter, 2023-Q4 to 2026-Q1. The quarterly rate rose from $1.30 (2024) to $1.50 (2025) to $1.73 (2026-Q1).

| Metric | AbbVie (ABBV) | Eli Lilly (LLY) |

| Latest Quarterly DPS (2026-Q1) | $1.73 | $1.73 |

| Prior Year Q1 DPS (2024-Q1) | $1.55 | $1.30 |

| Notable Quarter | Steady raises every year | Raised $1.30 to $1.50 to $1.73 |

| Forward Annual DPS | ~$6.92 | ~$6.92 |

| Forward Dividend Yield | ~2.7% | ~0.57% |

| Dividend Aristocrat | Yes (via Abbott heritage) | No |

If you’re an income investor, AbbVie’s yield of ~2.7% is real money coming into your account while you wait, and the history of regular increases makes it a good income builder. Lilly’s low yield is a conscious decision: to invest all the dollars we have in the growth machine. Neither is wrong. There’s just the fact that they are designed for different jobs. Investors can also compare these two with other large healthcare names such as UnitedHealth Group and Elevance Health. Check our detailed comparison here: UNH vs ELV stock in 2026.

Growth Drivers & Pipeline

The post-Humira revival of AbbVie’s stock is all about Skyrizi and Rinvoq, which are expected to bring in around $31.6 billion in 2026 revenue, enough to more than compensate for the losses from the biosimilars. AbbVie also supported its work in immunology in June 2026 with an acquisition of Apogee Therapeutics for some $10.9 billion.

APG777 (zumilokibart) is the lead compound in Apogee’s pipeline and is directed against the cytokine IL-13 in atopic dermatitis. The transaction is slated to close in Q3 2026, bringing an exciting early development stage pipeline to AbbVie’s portfolio.

So much simpler and so much louder is the story of Eli Lilly: GLP-1. Mounjaro sales increased by around 125% year over year in Q1 2026, while Zepbound sales increased by about 80%. Foundayo (orforglipron), approved on April 1, 2026, opens a much larger addressable market for patients who would rather not inject, as the first oral GLP-1 pill cleared for weight loss with no food or water restrictions. Revenue forecast for FY2026: AbbVie guides for $67.9 billion, while Lilly has raised its FY2026 forecast to $82-85 billion. The disparity in the growth rate is still large.

Risks of Investing in AbbVie and Eli Lilly Stocks

Honest investing starts with risks, not rewards.

| Risk Category | AbbVie (ABBV) | Eli Lilly (LLY) |

| Concentration | Skyrizi + Rinvoq dependence | Almost entirely GLP-1 class |

| Competition | Humira biosimilar erosion ongoing | Novo Nordisk + oral GLP-1 rivals |

| Pricing Pressure | Moderate; immunology stable | GLP-1 prices fell ~10% in Q1 2026 |

| M&A / Execution | Apogee deal ($10.9B) integration | Manufacturing capacity constraints |

| Valuation Risk | 8.6% implied perpetual growth needed | Rich ~27x P/E; little miss cushion |

The most overlooked risk for AbbVie: the company has a huge stack of past deal costs on which to earn a return, a key contributor to its modest 19.6% RNOA and to residual profit stalling since 2021.

The biggest underestimated risk for Lilly is a 10% decline in GLP-1 prices in Q1 2026, due to insurers and PBMs pushing back. The $1,208.12 per-share price today assumes perpetual growth of ~8.1%, which may prove too high; and if a rival GLP-1 takes share, the margin of safety is thin at ~27x forward earnings. For a different risk profile in healthcare, UNH’s intrinsic value analysis offers useful context.

The Verdict: Which Stock Is Right for You?

The honest answer depends entirely on the job you are hiring the stock to do.

| Investor Type | Better Fit | Why |

| Income / Dividend | AbbVie (ABBV) | ~2.7% yield vs. ~0.57%; paid to wait |

| Growth | Eli Lilly (LLY) | Fastest-growing franchise; GLP-1 dominance |

| Value (Low P/E) | AbbVie (ABBV) | Cheaper on traditional ratios (~15x vs. ~27x) |

| Expectations / ReOI Lens | Eli Lilly (LLY) | Embedded growth more achievable; RNOA 53.5% |

| Long-term (10Y+) | Eli Lilly (LLY) | Durable GLP-1 franchise + reinvestment runway |

Hire AbbVie, get paid and wait. It’s the more reliable hold with a ~2.7% forward yield, a lower valuation (~15x P/E) and a viable Humira succession plan. Simply look at the ReOI lens: AbbVie isn’t the deal it appears to be based on its forward P/E, as the company is being priced for more than the 8.6% profit growth it has left in its recent history.

Put Lilly on the back of a horse for growth, provided you can get through the bumps. Yes, it is valued at ~27x forward earnings and requires an 8.1% perpetual profit growth. That difficult bar, however, comes with a 53.5% RNOA, a profit base almost doubled in 2025, and one of the great business product cycles of modern times. The payout has a strong positive tilt if the GLP-1 business continues.

The trillion-dollar way to say it: AbbVie is priced for a recovery; Lilly is priced for a continuation. Choose the future that you think is true and make your job fit the situation, so you can survive if it is not. For readers interested in how these two stack up against another major player like Amgen, see our comparison: LLY vs ABBV vs AMGN.

Disclaimer

This article is for educational and informational purposes only and does not constitute financial, investment, or tax advice. It is not a recommendation to buy or sell any security. All figures reflect data available as of June 2026 and may change. Investing involves risk, including the possible loss of principal. Conduct your own research and consult a licensed financial professional before making any investment decision.

Frequently Asked Questions

Is AbbVie or Eli Lilly the better stock to buy in 2026?

It’s up to you to determine whether AbbVie (NYSE: ABBV) or Eli Lilly (NYSE: LLY) is the “better” company, based on your investment objectives. The steady dividend income and lower valuation make AbbVie the most attractive option for investors looking to earn regular payouts, while the booming cardiometabolic business (such as Mounjaro and Zepbound) makes Eli Lilly the more appealing choice for investors who like to buy growth.

Does AbbVie pay a better dividend than Eli Lilly?

Yes, by far around 2.7% forward yield compared to ~0.57% forward yield. AbbVie’s share price is far lower than Lilly’s, so its yield is roughly five times higher. For dividend income, there’s no question: it’s AbbVie.

Is Eli Lilly overvalued versus AbbVie?

LLY is trading at ~27x forward earnings versus ~15x for ABBV. The price demands 8.1% perpetual growth in Lilly’s profits, which is a lot, yet it’s supported by a 53.5% RNOA, that is accelerating rapidly. AbbVie demands 8.6% from a 19.6% RNOA. That is not a bargain on our lens.

Which has stronger growth: ABBV or LLY?

LLY. This revenue increase has come from the momentum of Mounjaro and Zepbound and has represented a ~56% increase in Q1 2026 revenue. The $82-85 billion is the FY26 guidance. AbbVie’s growth on the lower side of the double digits will be fueled by Skyrizi and Rinvoq. There’s still a huge divide in growth.

What are the biggest risks for each?

AbbVie: Biosimilar erosion on Humira, dependence on two immunology drugs and risk of Apogee integration execution. Eli Lilly: A rich stock valuation and a small buffer to failure, a single GLP-1 class concentration and ongoing pricing pressure from insurers and Novo Nordisk.

Is ABBV or LLY safer for a long-term investor?

AbbVie (ABBV) has a long history of dividends and has a more defensive stock profile, making it the more reliable option for long-term investors looking for income security and downside protection. But Eli Lilly (LLY) has better growth potential in its position as a leader in obesity and diabetes therapeutics.

References

- AbbVie Inc. (2026). AbbVie fourth quarter and full year 2025 financial results [Press release]. AbbVie Investor Relations. View Source

- AbbVie Inc. (2026). Form 10-K for fiscal year ended December 31, 2025. U.S. Securities and Exchange Commission. View Source

- Eli Lilly and Company. (2026). Lilly reports fourth-quarter and full-year 2025 financial results [Press release]. Lilly Investor Relations. View Source

- Eli Lilly and Company. (2026). Form 10-K for fiscal year ended December 31, 2025. U.S. Securities and Exchange Commission. View Source

- Eli Lilly and Company. (2026, April 1). FDA approves Lilly’s Foundayo (orforglipron) [Press release]. View Source

- AbbVie Inc. (2026, June 22). AbbVie to acquire Apogee Therapeutics for approximately $10.9 billion [Press release]. View Source

- U.S. Food and Drug Administration. (2026). Drug approvals and databases. View Source