By 2026, the Cheap Oil Stocks will be positioned to spill over in large amounts. Research about the underperforming energy business stocks whose cash flows are good, operating style is good, and their growth potential is also good.

Overview

The re-emerging interest in value-driven markets, with investors returning, is what is driving Cheap Oil Stocks. The past few years have seen capital flow biased toward growth and technology, with good energy companies trading at lower valuations than their cash flows and asset support warrant. This is why price is not correlated with intrinsic value, which makes undervalued energy stocks in 2026 a compelling addition to a portfolio in the long run. Firms that are well operationalised are normally re-rated higher when oil demand stabilises and supply becomes constrained.

Research has shown that when sentiment is low, traditional energy is mispriced, offering good entry points for value investors (SeekingAlpha, 2025).

Besides a valuation appeal, the structural position of oil in the global economy continues to drive demand. The bulk of the infrastructure development, driven by petroleum, airlines, shipping, chemical industries, and agriculture, cannot be migrated to conventional energy in the near future (ECMarkets, 2025). This creates an effective bottom-base demand in most macro conditions.

If investors are seeking cheap oil stocks to buy, they will most of the time focus on firms with the ability to convert working capital into long-term earnings rather than investing in the volatility of commodities. It is here that RNOA comes in. It emphasises operational discipline, asset productivity, and efficiency, and helps distinguish between companies that survive only through the cycles and those prepared to grow through them. The analysis that follows is an analysis of five companies, namely COP, EOG, XOM, ENB and EPD, as per RNOA performance data as an indicator of long-term strength of investments.

Why RNOA Matters When Evaluating Cheap Oil Stocks

RNOA is also relevant, especially when analysing Cheap Oil Stocks, as not all companies can achieve economic profit at the same rate. Two firms could achieve the same level of revenue, yet the company that would achieve a greater payoff on net operating resources is using its wells, pipelines, and infrastructure more productively. This means it will generate more revenue with fewer resources, which would otherwise translate into higher free cash flow, higher dividend yields, and survival during difficult situations. The trend in RNOA is a positive sign, as it suggests the discipline in operation is growing, but a negative trend could signal cost increases, reduced production, or ineffective capital distribution.

To give credit to investors, RNOA will be used to filter out stocks that really look interesting, cheap oil, and those that only seem interesting because they perform badly. When a business has recorded a good or improving RNOA even as crude prices fluctuate, it is a good sign and not just an accident. No wonder analysts have a tendency to use RNOA to predict the low-valuation oil producers’ long-term competitiveness, in addition to defining which names would perform better were a positive energy market forecast for 2026. Additionally, in brief, RNOA helps identify underestimated energy reserves with operating quality that enable them to survive cycles and remunerate patient shareholders.

RNOA Trend Analysis

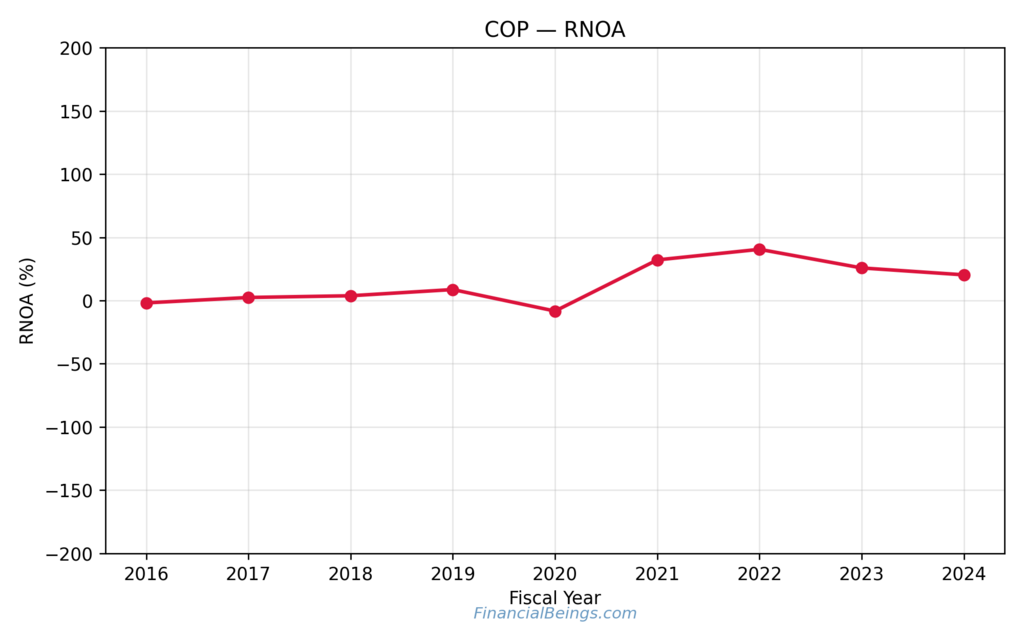

ConocoPhillips (COP)

| Year | RNOA % |

| 2016 | -1 |

| 2017 | 3 |

| 2018 | 4 |

| 2019 | 9 |

| 2020 | -8 |

| 2021 | 32 |

| 2022 | 41 |

| 2023 | 27 |

| 2024 | 21 |

Figure 1. RNOA Trend for ConocoPhillips (2016–2024)

COP is associated with rebound strength. RNOA returned in 2022 with a robust recovery of 41% from 2020, when it was at -8, amid favourable crude prices. It is a performance that makes COP a high-upside energy stock to the cyclical investors. Scalability may be indicated when market performance is defined by peak-year performance.

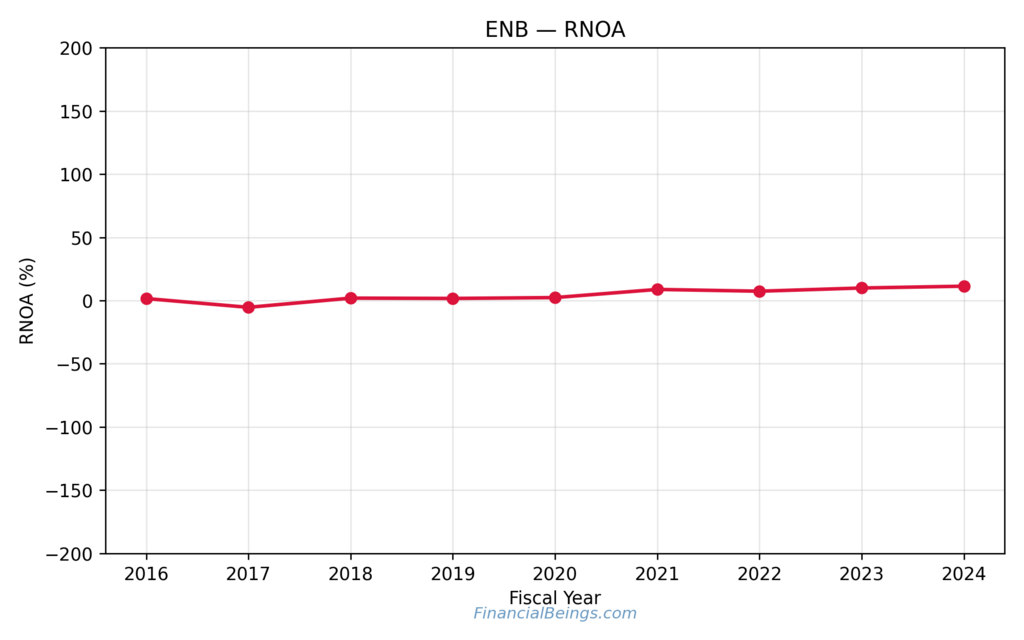

Enbridge (ENB)

| Year | RNOA % |

| 2016 | 2 |

| 2017 | -5 |

| 2018 | 1 |

| 2019 | 1 |

| 2020 | 2 |

| 2021 | 8 |

| 2022 | 7 |

| 2023 | 9 |

| 2024 | 11 |

Figure 2. RNOA Trend for Enbridge (2016–2024)

ENB is not volatile as an upstream peer. The slow yet consistent growth rate of 2% to 11% in 2016 and 2024, respectively, represents stable cash flow for the pipeline. Midstream infrastructure returns provide little information about crude oil prices. ENB is a recommended income portfolio for investors seeking long-term oil investment ideas with lower risk.

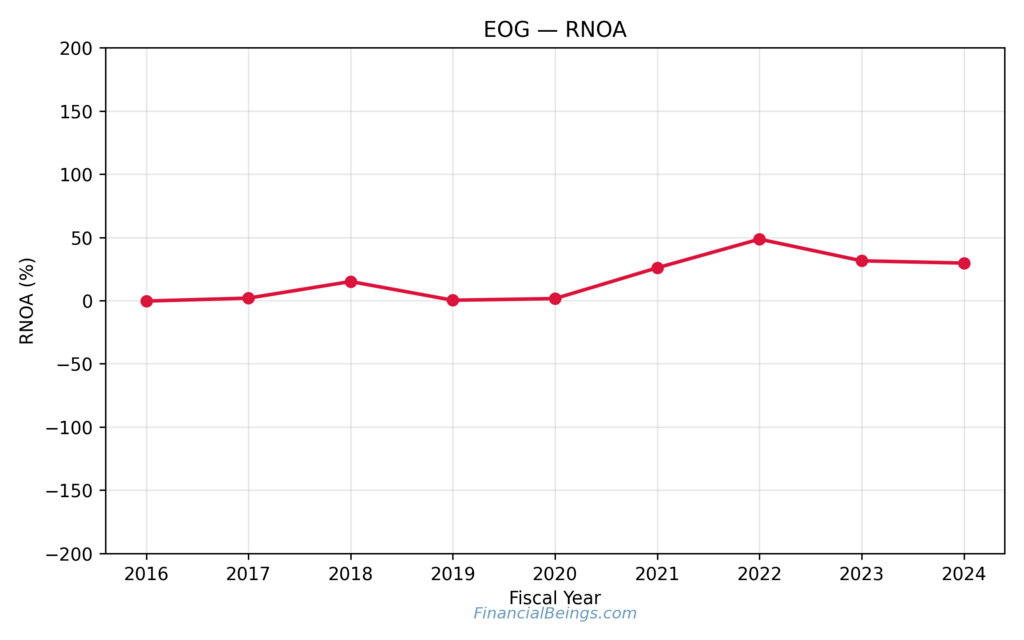

EOG Resources (EOG)

| Year | RNOA % |

| 2016 | 1 |

| 2017 | 3 |

| 2018 | 17 |

| 2019 | 1 |

| 2020 | 2 |

| 2021 | 26 |

| 2022 | 48 |

| 2023 | 33 |

| 2024 | 31 |

Figure 3. RNOA Trend for EOG Resources (2016–2024)

EOG dominates in efficiency. RNOA in 2022 also rose to 48%, the highest among all the companies considered. It also leads the best oil and gas value stocks in terms of operational excellence, low breakevens, and shale cost discipline (Yahoo Finance, 2024). EOG would suit investors seeking aggressive growth prospects.

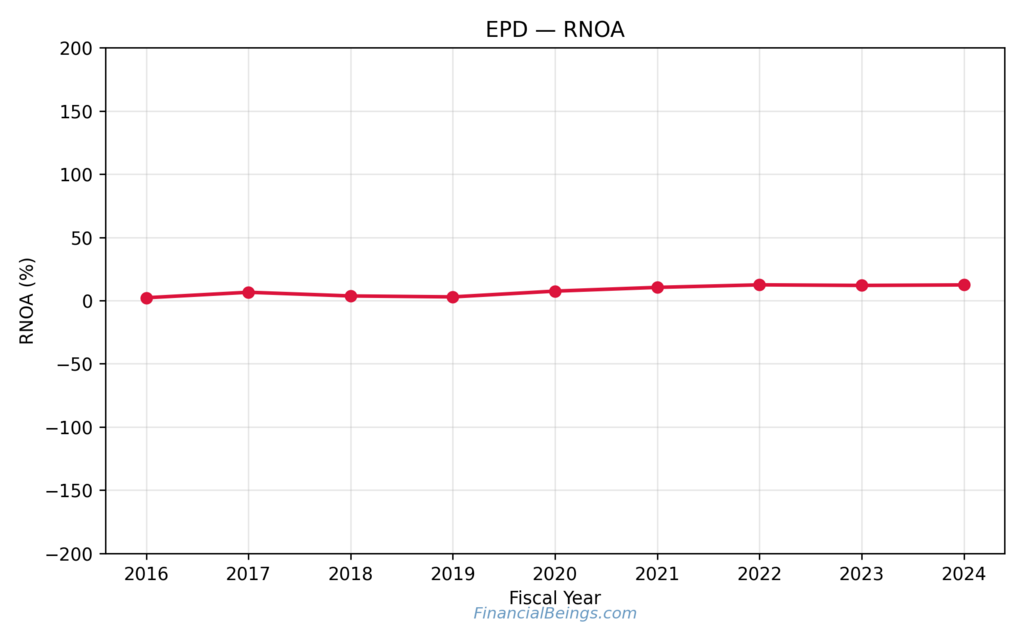

Enterprise Products Partners (EPD)

| Year | RNOA % |

| 2016 | 2 |

| 2017 | 7 |

| 2018 | 4 |

| 2019 | 3 |

| 2020 | 8 |

| 2021 | 11 |

| 2022 | 13 |

| 2023 | 13 |

| 2024 | 14 |

Figure 4. RNOA Trend for Enterprise Products Partners (2016–2024)

From 2016 to 2024, GDP increased by 2 per cent to 14 per cent, and stable delivery. Midstream assets include the repeated turnover of transportation and storage and are not exposed to spot prices (Nasdaq Market Insight, 2024). This has positioned EPD as one of the low-PE oil and gas companies that passive dividend-income investors are interested in.

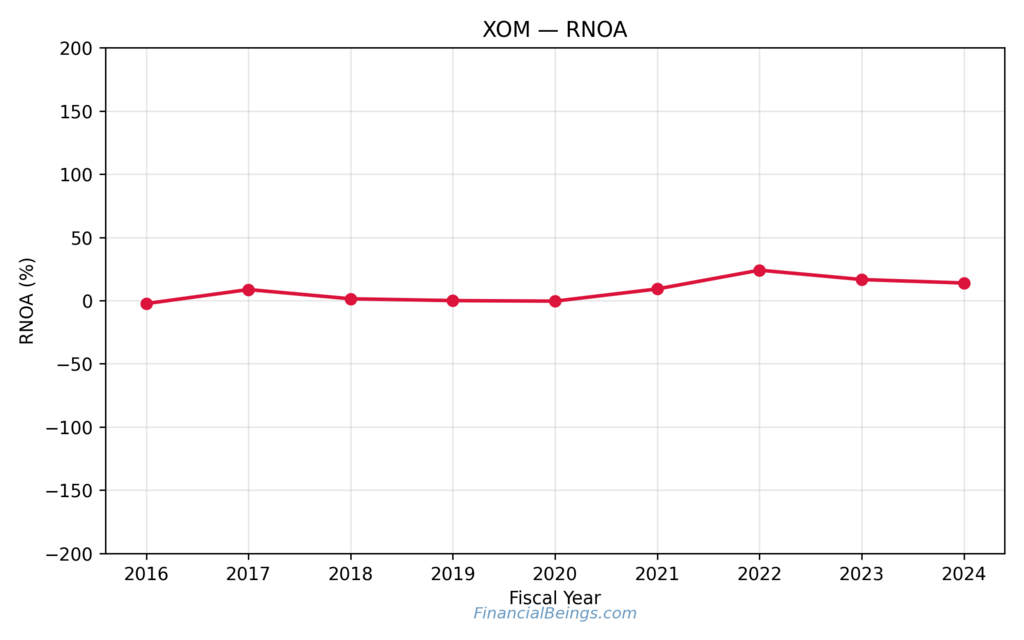

Exxon Mobil (XOM)

| Year | RNOA % |

| 2016 | -2 |

| 2017 | 9 |

| 2018 | 3 |

| 2019 | 1 |

| 2020 | 0 |

| 2021 | 9 |

| 2022 | 24 |

| 2023 | 17 |

| 2024 | 14 |

Figure 5. RNOA Trend for Exxon Mobil (2016–2024)

XOM is yet an equal oil major. The change in RNOA was near 0% to 24% in 2020 and 2022, respectively. It has also combined upstream, refining, petrochemicals, and global assets, which makes it a lower-risk compared to pure E&P names. XOM is a good investment for balanced investors who do not like aggressive volatility but prefer stability.

Comparative Insight

| Company | Peak RNOA | Nature |

| EOG | 48% | High return, high potential |

| COP | 41% | Cyclical rebound leader |

| XOM | 24% | Balanced cash-flow model |

| EPD | 14% | Stable midstream income |

| ENB | 11% | Long-term infrastructure play |

The investors often use the blend allocation in the pursuit of oil sector deep-value picks:

These high RNOA will imply that the companies are at a different strategic position in a portfolio. When oil markets are healthy, EOG and COP offer the highest return potential and are therefore attractive to investors seeking growth and undervalued stocks. XOM is ideally positioned as an integrated company with sustained refining and chemicals operations, as well as midstream and upstream operations. On the other hand, EPD and ENB generate consistent income in the midstream, and cash flows are supported by pipeline and transport contracts, unlike the unpredictability of oil prices. It is this difference that leads investors to accord them different names: some are drivers of returns, while others are drivers of income stabilisers.

Investors tend to select a mixed portfolio for those characteristics, seeking deep-value stocks in the oil industry without overreliance on a single stock. Balancing XOM, EPD, and ENB creates equilibrium and provides income, while COP or EOG provides acceleration upside and a rise in crude prices. Such diversification makes volatility null and provides multiple drivers of returns across cycles, enabling portfolios to hold up well during a downturn and to gain during periods when commodity markets perform well.

Further Reading : Best Stocks to Buy for Long Term Growth Before 2025 Ends, Not Just Tech Stocks!

Further Reading : APA vs. ConocoPhillips (COP): Which Oil Stock Offers Better Value in 2025?

Further Reading : ConocoPhillips Stock Forecast 2025: Can COP Outperform as Oil Prices Cool?

Why 2026 Could Be a Breakout Year for Cheap Oil Stocks

The energy companies are trading at reasonable multiples. The slow rise of the price floor is due to the recovery in the global environment, and the demand is even. Good oil stocks that are poised to appreciate in the long run may rise as capital returns to energy. The visibility of shareholders is assured through dividend and buyback increases (ECMarkets, 2025).

As long as the crude does not decline, undervalued energy stocks in 2026 will have a significant rerate, especially cost-disciplined. The crude oil demand outlook for 2026 is not high, as individuals will not abandon their industrial and transport consumption (Morningstar, 2024).

Risks to Consider

There are several risks involved in investing in oil which investors must consider before investing capital. The biggest risk is commodity price volatility, especially among upstream producers like EOG and COP. They make more or less profit depending on crude prices, which can be volatile during international crises, due to OPEC decisions, or during economic crises, leading to a decline in demand. In addition to price risk, regulatory pressure is increasing, and governments are promoting decarbonization, EVs, and emissions policies.

Research stresses that ESG-related restrictions may reduce the appeal of long-term investments in fossil fuels (MDPI ESG Risk Paper, 2024). This could limit project approvals, increase compliance costs, or cripple production growth. Market sentiment is also in charge of it. Fundamentals are good, with energy that can be undervalued in the long run, as investors will flock to tech, renewables, or other narratives.

However, these challenges, downturns in oil to provide attractive entry points to patient value investors. Historically, the majority of long-term returns in the energy sector were best during pessimistic cycles when stock prices were below fair value and cash flows were unaffected. Intermediary companies like ENB and EPD mitigate risk by offering fee-based sources of revenue that remain stable even in poor pricing conditions, thereby providing portfolio stability. On the other hand, high-paying producers like COP and EOG become the majority profitable as the cycles resume growing.

Conclusion

The Cheap Oil Stocks themselves remain neglected in contrast to the fast-moving technology industries, yet the financial welfare of the majority of oil corporations has been improving by accident. The 2016-2024 trends of RNOA show that the operation profits have been volatilized in the post-2021 cycle, and in particular with the upstream players. The EOG and COP turn out to be good sources of returns and perform well when crude prices are high, whereas the EPD and ENB provide consistent midstream income, even during periods when commodities are declining.

XOM is placed in the centre of the line between size, diversification, and constant cash flow, and therefore, it is one of the main anchor holdings in most portfolios.

An array of these names will lower downside risk and increase exposure to a range of drivers of returns for investors seeking cheap oil stocks to buy now. Growth stocks like COP and EOG rise with booming markets, while ENB and EPD offer a steady dividend yield. XOM manages the portfolio as a diversified energy investment worldwide. These undervalued energy stocks in 2026 may be rewarded in the long run, given attractively valued cash flows as the mood moves back to value and crude prices improve.

All calculations and valuation estimates are FinancialBeings’ own, based on data sourced from SEC filings (10K and 10Q), use or reproduction before prior approval is prohibited.

Frequentlay Asked Questions (FAQs)

What is the most undervalued oil stock?

The most undervalued term depends on the type of returns an investor wishes to achieve. EPD and ENB appear to be undervalued in terms of cash flow and income, which is why they are the more preferable choices for stability and yield. EOG and COP seem to be underrated in growth and RNOA efficiency, especially in efficient crude cycles. They also contribute to good in different ways, and thus they have to be selected on the basis of income vs growth preferences. However, we rate EOG and COP as the undervalued opportunities.

Which oil share is best?

There is no single best oil stock for any investor. Among them, XOM is the most appropriate, as it is a global corporation with diverse sources of income. Investors who prioritise dividends and stability can use ENB or EPD, but not the rest, and this is where EOG or COP can be a better addition to undervalued growth-oriented portfolios.

What factors affect oil stock prices?

Oil stock prices are driven by crude oil prices, supply and demand, and global economic conditions. Geopolitical events, OPEC decisions, and company performance also play a key role.

Can beginners invest in cheap oil stocks safely?

Yes, beginners can invest in cheap oil stocks, but they should start carefully by researching companies, diversifying investments, and understanding market risks. Since oil stocks can be volatile, it’s important to invest small amounts and focus on long-term strategies.

What is the best time to invest in oil stocks?

The best time to invest in oil stocks is when oil prices are low or during market downturns, as this can offer better entry points. Investors also look for periods of rising demand or economic recovery, which can drive oil prices and stock values higher.

Usama Ali

Usama Ali is the founder of Financial Beings and a self-taught investor who blends classic valuation study with insights from psychology. Inspired by works from Benjamin Graham, Aswath Damodaran, Stephen Penman, Daniel Kahneman, and Morgan Housel, he shares independent, data-driven research to help readers connect money, mind, and happiness.

Disclaimer

The content provided herein is for informational purposes only and should not be construed as financial, investment, or other professional advice. It does not constitute a recommendation or an offer to buy or sell any financial instruments. The company accepts no responsibility for any loss or damage incurred as a result of reliance on the information provided. We strongly encourage consulting with a qualified financial advisor before making any investment decisions.