A future-based valuation analysis of the UnitedHealth. This discussion unravels the drivers of sustainable growth, risk-adjusted fundamentals, and multi-year fair-value targets in order to understand where UNH would be in 2025 and beyond.

Overview

What Is the Intrinsic Value of UNH Stock? UnitedHealth is one of the most powerful brands in the healthcare industry. It is big, profitable and well-managed. It is followed by investors due to a long history of a stable increase in revenue, earnings, and cash flow at the company. At times such as these, when markets become noisy, most investors will go back to the same question.

This is not to be found in the short-run fluctuations of the market. Rather, it is based on the basics that define the long-term values of UnitedHealth. They are the magnitude of its operating assets, its earnings power stability, and the returns it gives on its core business. These indicators show the quality of the business in terms of transforming premiums, services and operating assets to real economic value.

The analysis of these areas eliminates hype and makes the analysis based on the facts of the public filings of the company. The annual reports of UnitedHealth reveal that over a long period, the revenues and a high level of operating income have been growing steadily (UnitedHealth Group, 2025).

UnitedHealth’s Business in Simple Terms

UnitedHealth is a massive health services and health benefits platform. The two primary arms are UnitedHealthcare and Optum. UnitedHealthcare is involved in insurance and benefits. Optum is a health delivery, analytics and pharmacy services (Reuters, 2025).

This mixture presents the group with an assortment of revenue streams. There is insurance which is linked to predictable premiums. Optum incorporates increased lucrative service and technology revenues. It is this combination that, over time, has produced the majority of the UnitedHealth intrinsic value calculation models of UnitedHealth, because it fosters growth and sustainability (Morningstar, 2025a).

The annual reports indicate that the revenue of UnitedHealth was more than 400 billion dollars in 2024, as compared to the revenue of about 371.6 billion dollars in 2023 (UnitedHealth Group, 2025; Macrotrends, 2025b). This high growth of the top line is a continuum of positive growth that adds to the UnitedHealth long-term valuation perspective.

Net Operating Assets and Operating Liabilities

A good intrinsic value model for UNH starts with the operating base.

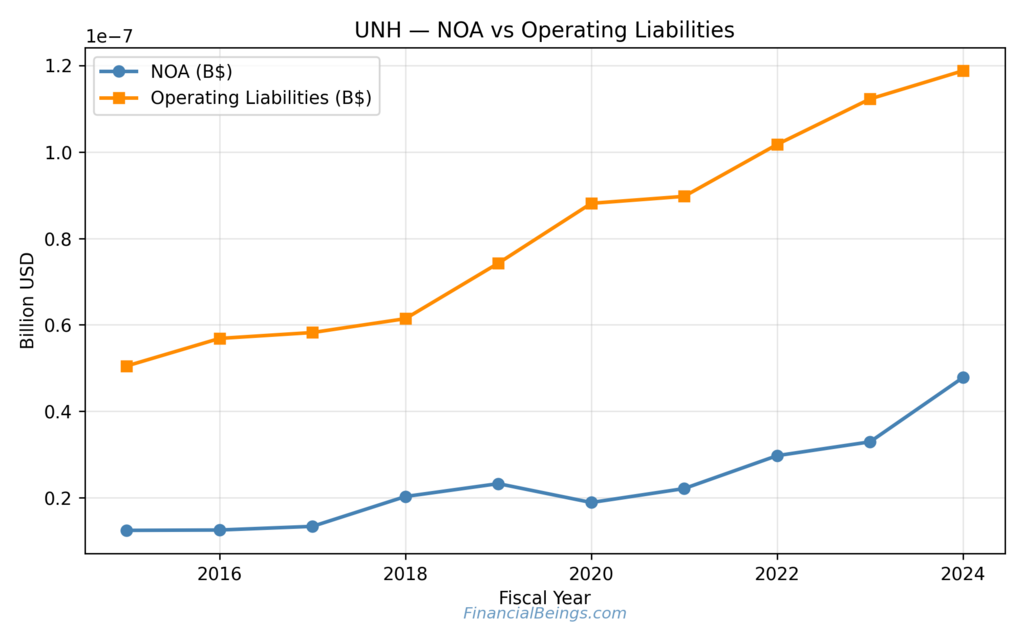

Figure 1. UnitedHealth Net Operating Assets vs Operating Liabilities, 2015–2024.

Table 1. NOA And Operating Liabilities

| Fiscal Year | NOA (B$) | Operating Liabilities (B$) |

| 2015 | 0.1 | 0.5 |

| 2016 | 0.1 | 0.6 |

| 2017 | 0.1 | 0.6 |

| 2018 | 0.2 | 0.6 |

| 2019 | 0.2 | 0.7 |

| 2020 | 0.2 | 0.9 |

| 2021 | 0.2 | 0.9 |

| 2022 | 0.3 | 1.0 |

| 2023 | 0.3 | 1.1 |

| 2024 | 0.5 | 1.2 |

This is a significant trend to investors. Growth in the bottom of NOA means that the company is still investing in the business. In the event that such a base is providing good returns, then it will have high sustained intrinsic value. In the majority of intrinsic value of UNH models, the growth of NOA is a sign that the franchise is not stagnant, but rather growing. We have reviewed UNH in 2026 for long-term investors, you can find our latest study here, “UNH Stock 5 Year Forecast: Long-Term Outlook, Valuation Scenarios, and Key Risks (2026–2030)“

Residual Earnings and the Earnings Path

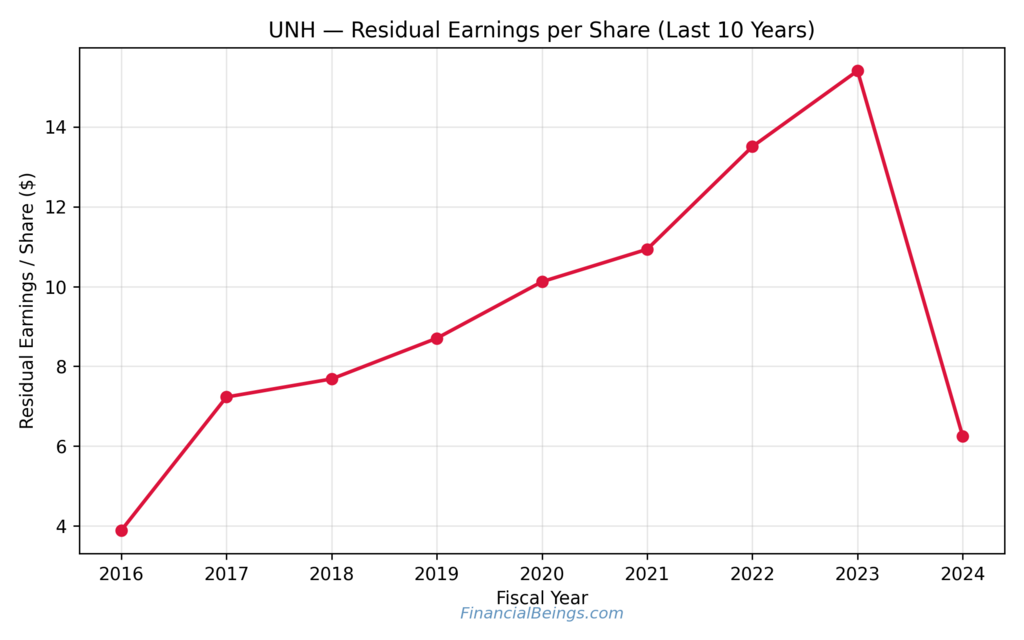

The residual earnings are profit after deduction of the cost of capital. They can be used with long-term value models.

Figure 2. UnitedHealth Residual Earnings per Share, 2016–2024.

Table 2. Residual Earnings Per Share

| Year | Residual EPS ($) |

| 2016 | 3.9 |

| 2017 | 7.2 |

| 2018 | 7.7 |

| 2019 | 8.7 |

| 2020 | 10.1 |

| 2021 | 10.9 |

| 2022 | 13.5 |

| 2023 | 15.3 |

| 2024 | 6.2 |

The government programs may also be strained and higher medical cost ratios in 2024, which may have led to that dip (UnitedHealth Group, 2025).

The bigger picture is healthy for the long-term investors who track the trend of the UnitedHealth earnings trajectory. The entire period of the residual earnings shows a strong growth of compound. This trend will tend to prefer a premium valuation multiple in the minds of most investors, should it stabilise again.

Return On Net Operating Assets (RNOA)

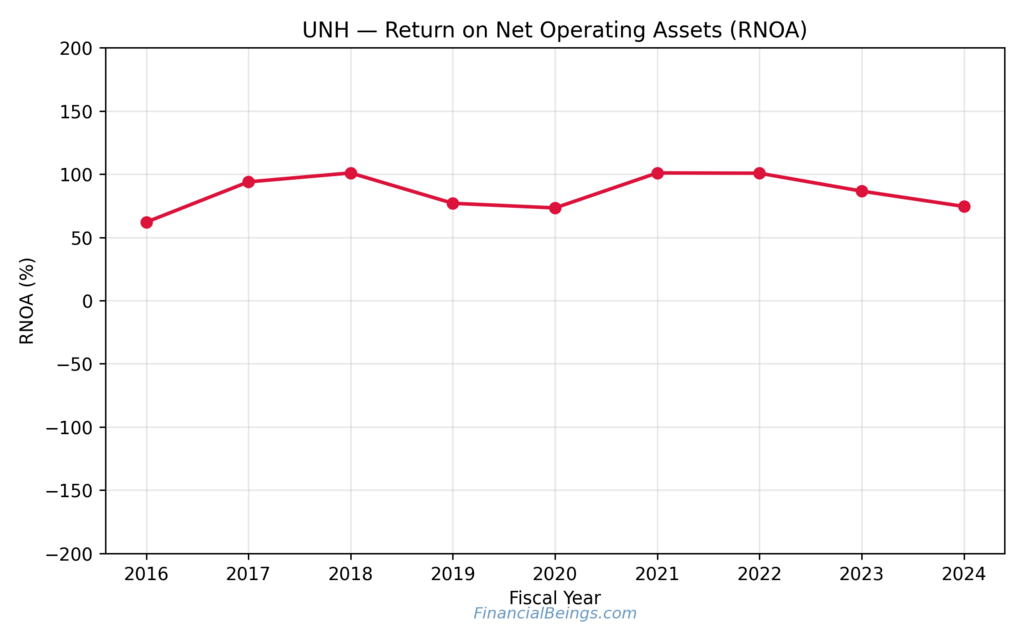

RNOA informs us about the amount of ROA of the company on its operating base but not including financial leverage.

Figure 3. UnitedHealth Return on Net Operating Assets (RNOA), 2016–2024.

Table 3. RNOA (%)

| Year | RNOA (%) |

| 2016 | 62 |

| 2017 | 95 |

| 2018 | 101 |

| 2019 | 78 |

| 2020 | 73 |

| 2021 | 101 |

| 2022 | 101 |

| 2023 | 88 |

| 2024 | 75 |

The high and constant operating returns can be justified by the past financial statements as offered by Macrotrends and the 10-K statements of the organisation (Macrotrends, 2025a; UnitedHealth Group, 2025).

This is among the primary factors for an investor. When a company is generating high rates of returns on its net operating assets, then it does not need to seek excessive growth in the process of creating value. The latter is central to answering What Is the Intrinsic Value of UNH Stock, as high RNOA can be the only reason to reply with a higher fair value than would be implied by a simple book-value model.

Connecting These Metrics to Intrinsic Value

A combination of many factors will be one of the realistic valuation of UnitedHealth:

- Growth in NOA

- Long-run residual earnings

- Stable RNOA

- Consistent free cash flow

- Balance sheet strength

As financial reports have it, the operating income has remained stagnant at the low 30 billion dollar range within the last several years, despite the variable medical cost trend (Macrotrends, 2025c). According to the 10-K and quarterly reports, the level of cash generation is high (UnitedHealth Group, 2025; UnitedHealth Group, 2024).

Growth And Profitability Outlook

Without numeric estimates, we can analyse the drivers which define the UNH growth and profitability outlook.

Stable membership and premium base.

UnitedHealth caters to tens of millions of people, operating on commercial plans, on Medicare, and on Medicaid plans (UnitedHealth Group, 2025). Massive membership gives it the scale and bargaining power.

Optum’s contribution

According to both Reuters and Morningstar, Optum is among the earnings generators, and its services in the sphere of care delivery, pharmacy benefits and analytics (Reuters, 2025; Morningstar, 2025a). This constituent would be more profitable compared to pure insurance.

Cash flow and capital returns.

Yahoo Finance claims that UnitedHealth has a long record of buying back shares and dividends that it has continually been paying in regular portions using steady cash flows (Yahoo Finance, 2025a). The assumption of many long-term UnitedHealth valuations is the reason behind the intrinsic value in the slow growth, which is a discipline.

Revenue trend

According to Macrotrends data, annual revenue will grow by 2024, which was below 200 billion dollars ten years ago and will reach approximately 400.3 billion dollars (Macrotrends, 2025b). Such a continued trend makes it stronger to possess a constructive UnitedHealth long-horizon fair value view.

Risk-Adjusted Return Profile

It is impossible to make a complete valuation without having a glance at risk.

Key risks include:

- Higher medical cost ratios.

- Regulatory changes in Medicare Advantage and Medicaid.

- Competitive prices through peer-to-peer.

- Cybersecurity and technology spending.

- Integration risk as Optum is still growing.

The recent revelation and reporting on the topic of finances reiterate the stress that is being caused by the rising workload of medical care, especially in government programs (UnitedHealth Group, 2025; Reuters, 2025).

At the same time, the balance sheet of the company is healthy, and its level of operating income is healthy, which indicates a healthy UNH risk-adjusted return analysis (Morningstar, 2025b; Macrotrends, 2025c).

Many long-term investors are not as interested in the absence of risk in their investments. It is how the company manages such risks over the long term.

How Past Market Behaviour Guides Today’s View

History does not repeat, but it may inform interpretation.

UnitedHealth’s share price has been in a sequence of drawdowns, yet the trend of the long term is very positive in the last fifteen years (Macrotrends, 2025d). The same is depicted in the trend of Yahoo Finance price history, which has even more highs in the cycles (Yahoo Finance, 2025a).

The stock has since been revived because stabilised outcomes have occurred in a string of panics in the past due to the medical cost spikes or policy changes. Many investors still cannot forget those episodes when they look at the perspective of UNH stock fair value 2025 outlook today. They know that the path can be bumpy, but the franchise has already gone through shocks.

Multi-Year Drivers That Shape Fair Value

The structural forces and not accurate numbers will form the valuation of the future that is forward-looking and yet will be consistent with the past.

Key drivers include:

Ageing population

The ageing populations augment the healthcare and insurance requirements. UnitedHealth has a very large book of Medicare, and it, thus, makes the company vulnerable to this trend (UnitedHealth Group, 2025).

Integrated care delivery

Optum clinics, pharmacy and data tools are aimed at improving the outcomes and keeping costs down. It is applicable to maintain the margins and develop relationships with customers in the long run (Reuters, 2025; Morningstar, 2025a).

Scale and data advantages

UnitedHealth is less expensive than smaller counterparts in the fact that huge enrolment and claims data are critical to long-term worth (Morningstar, 2025b).

Capital allocation discipline.

The management has been reported to invest in the business over the years, making certain deals, and returning money to shareholders in a slow way (UnitedHealth Group, 2025; Yahoo Finance, 2025a).

It is these forces that set the basis of all healthcare mega-cap valuation forecasts on UnitedHealth.

Further Reading : UNH Stock Forecast 2025: Promising Insights and Projections from Industry Experts!

Investor Point of View

It is based on figures, yet investor behaviour is also a consideration.

A typical long-term investor can state:

- I would like a company that will grow even through times of recessions.

- UnitedHealth has ensured that revenue and earnings continue to grow for several years.

- The combination of UnitedHealthcare and Optum is not easy to copy, as it is.

This is expressed in the many analyst reports and stock projections summaries like Morningstar, Yahoo Finance, and Reuters (Morningstar, 2025a; Yahoo Finance, 2025a; Reuters, 2025).

Conclusion

The combination of scale, enormous returns on operating assets, and years of uninterrupted growth are offered by the company, UnitedHealth. Both the data of the NOA, the residual earnings and RNOA are moving in the same direction. The only apparent setback that the company has experienced is in 2024, and has built high value on the capital which it utilizes.

The filings and financial databases published by the company show the image of the company that still records the high level of revenue, the high level of operating income, and the high level of cash flow even in tough conditions (UnitedHealth Group, 2025; Macrotrends, 2025b; Macrotrends, 2025c).

This is a definite conclusion for many investors. What is the Intrinsic Value of UNH Stock considered through the long prism? As long as UnitedHealth is not losing its high returns on its growing operating asset base, its intrinsic value will likely remain above that of an average insurer with worse economics.

All calculations and valuation estimates are FinancialBeings’ own, based on data sourced from SEC filings (10K and 10Q), use or reproduction before prior approval is prohibited.

Frequently Asked Questions (FAQs)

Is UNH stock overvalued?

At one time, UNH has been trading at a premium as its investors feel that the cash flow and operating returns are very stable. The valuation will be based on the model adopted, but a time test of history has revealed that the company has been capable of making good returns on its operating assets over many years. This consistency is the reason why some investors feel that it is highly rated among other insurers.

What is the intrinsic value of UNH stock?

The market is expecting around 4% long term growth in UnitedHealth Group Inc. (UNH). At the current price, the return for investing in UNH is around 10.5%. However, we expect the market growth expectations to shift to a higher level and thus the return for investors can surpass 11.5% and thus a high share value between $362 – $426. The company is intrinsically rated in relation to the operating assets, residual earnings and long-term on net operating assets. All this basic leads to the point that UnitedHealth has a better economic background and consistent earnings per share, which can be considered as positive long-term valuation and in the long run we see upside.

Did Warren Buffett buy UNH?

In the past years, Warren Buffett has been extremely conservative about the stock market. But in the last quarter, he has acquired Chevron (NYSE: CVX), UnitedHealth Group (NYSE: UNH) and Pool Corp (NASDAQ: POOL). The bulk of investors would be scared to buy the dip, yet Buffett sees the opportunity to acquire the largest health insurance company in America with a massive discount. He purchased 5.049 million shares of UNH stock during Q2 2025. It is now worth $1.57 billion (Yahoo Finance, 2025a).

Usama Ali

Usama Ali is the founder of Financial Beings and a self-taught investor who blends classic valuation study with insights from psychology. Inspired by works from Benjamin Graham, Aswath Damodaran, Stephen Penman, Daniel Kahneman, and Morgan Housel, he shares independent, data-driven research to help readers connect money, mind, and happiness.

Disclaimer

The content provided herein is for informational purposes only and should not be construed as financial, investment, or other professional advice. It does not constitute a recommendation or an offer to buy or sell any financial instruments. The company accepts no responsibility for any loss or damage incurred as a result of reliance on the information provided. We strongly encourage consulting with a qualified financial advisor before making any investment decisions.